Impact of Ports’ Diversification-Driven Industrial Transformation on Operating Performance: Regulatory Effect of Port Cities’ Urban Economic Development Level

Abstract

:1. Introduction

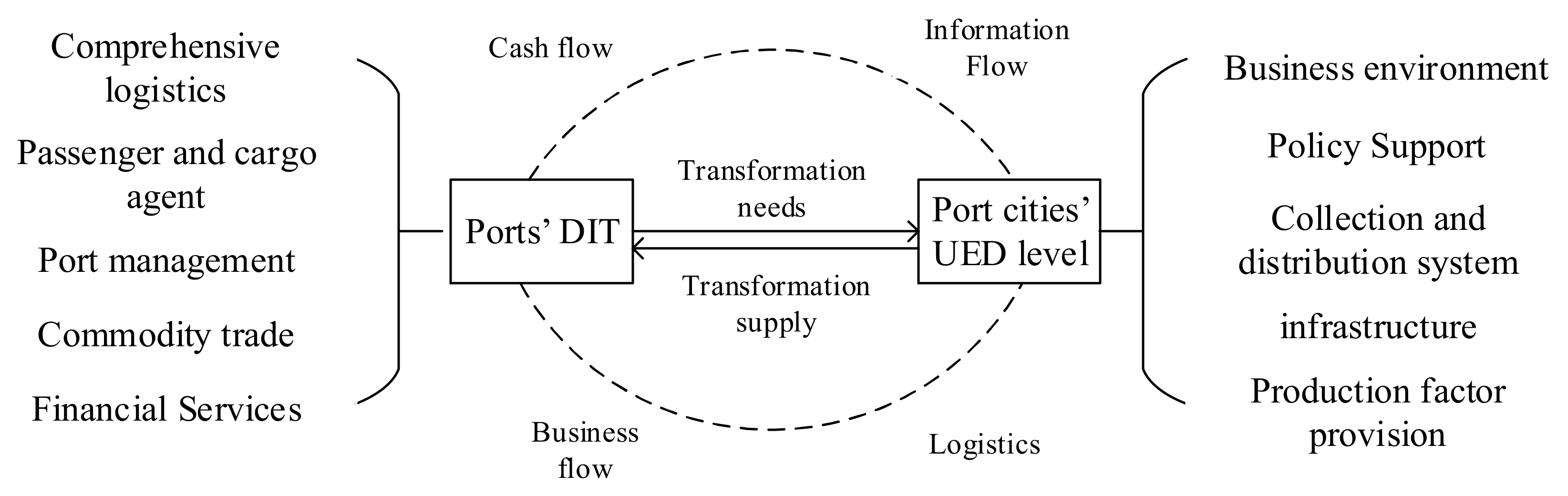

2. Literature Review and Research Hypotheses

3. Research Design

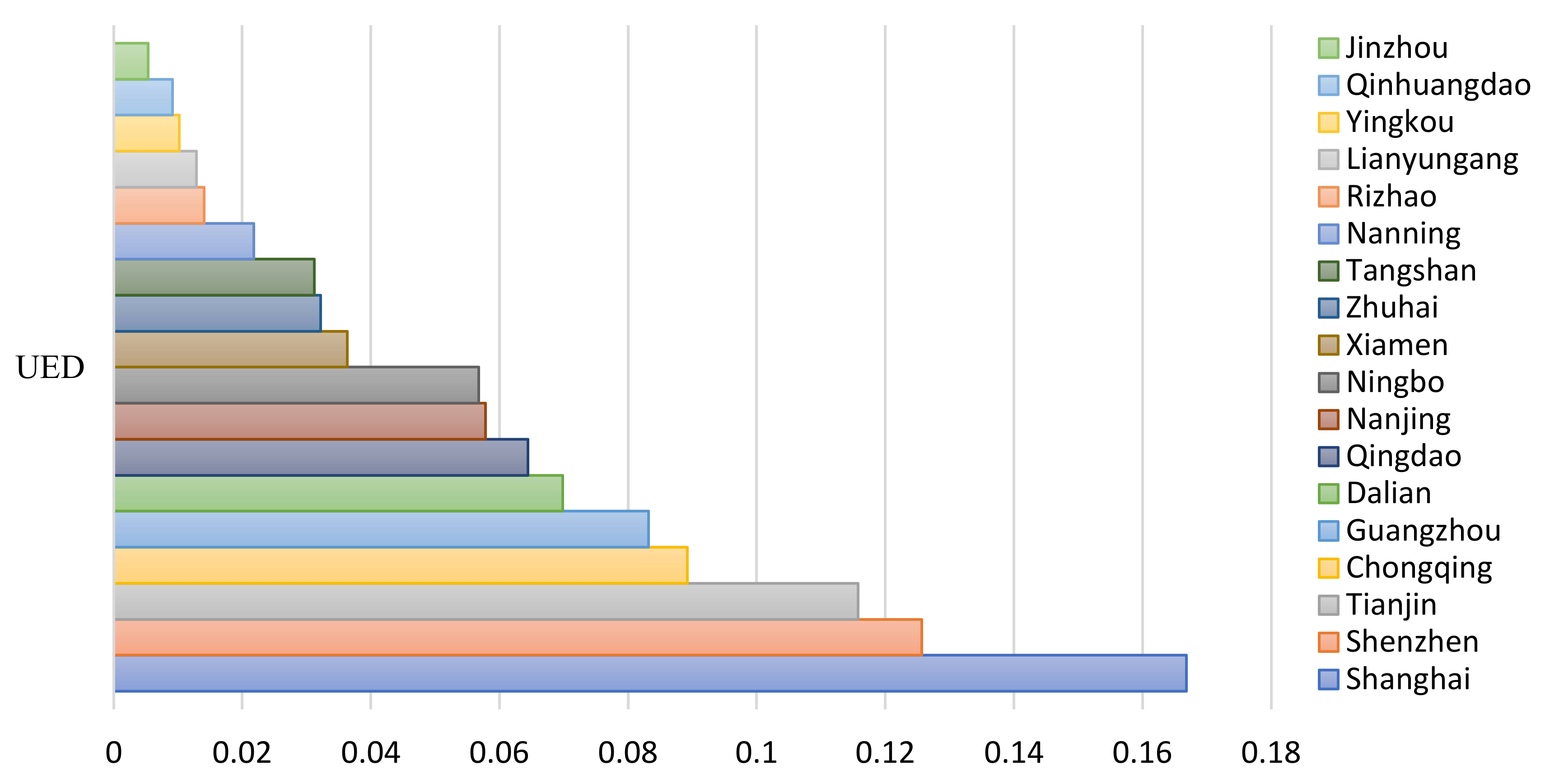

3.1. Sample Selection and Data Sources

3.2. Measurement of Variables

3.2.1. Indicators for Measurement of DIT

3.2.2. Indicators for Evaluating the UED Level of Port Cities

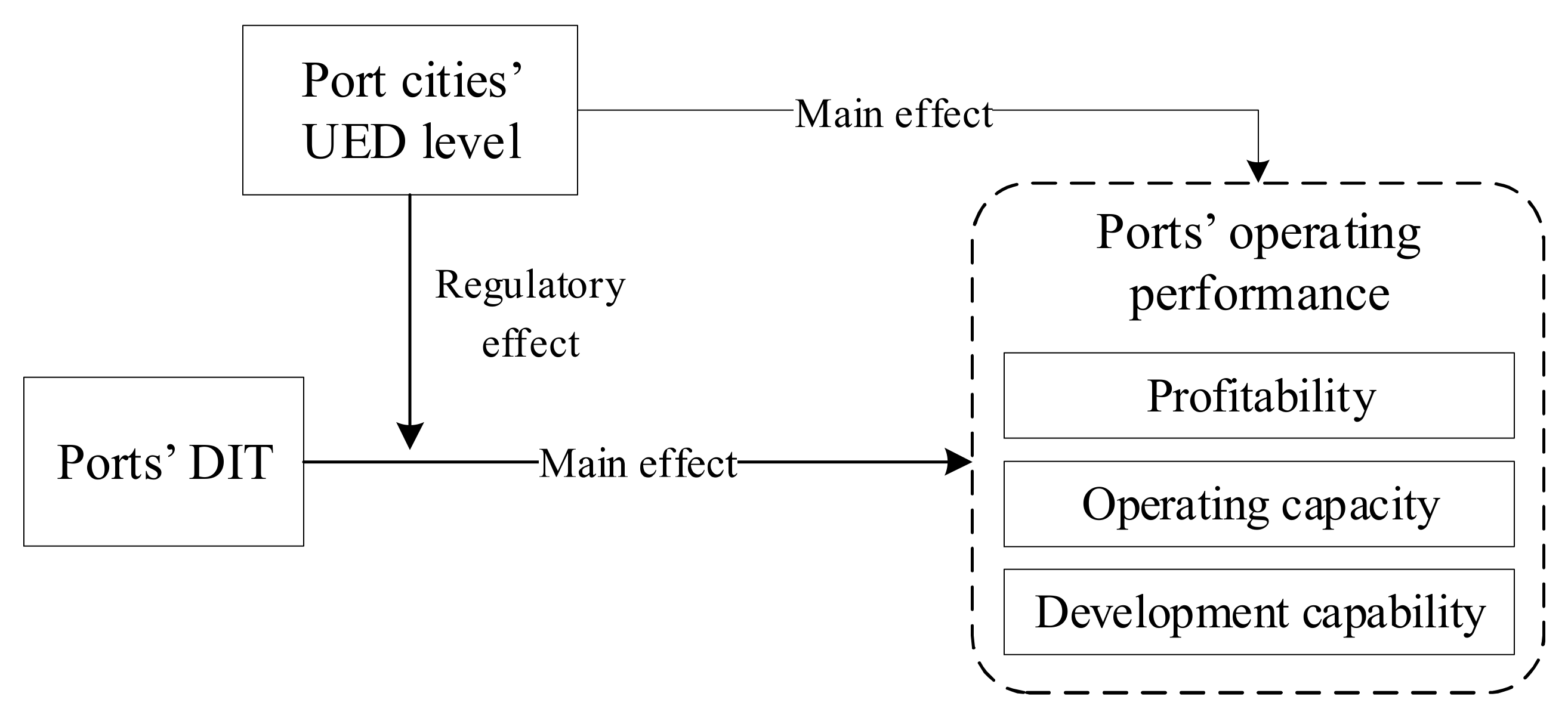

3.2.3. Indicators for Measuring the Operating Performance of Port Enterprises

3.2.4. Control Variables

3.3. Model Building

4. Results of Empirical Analysis

4.1. Descriptive Analysis

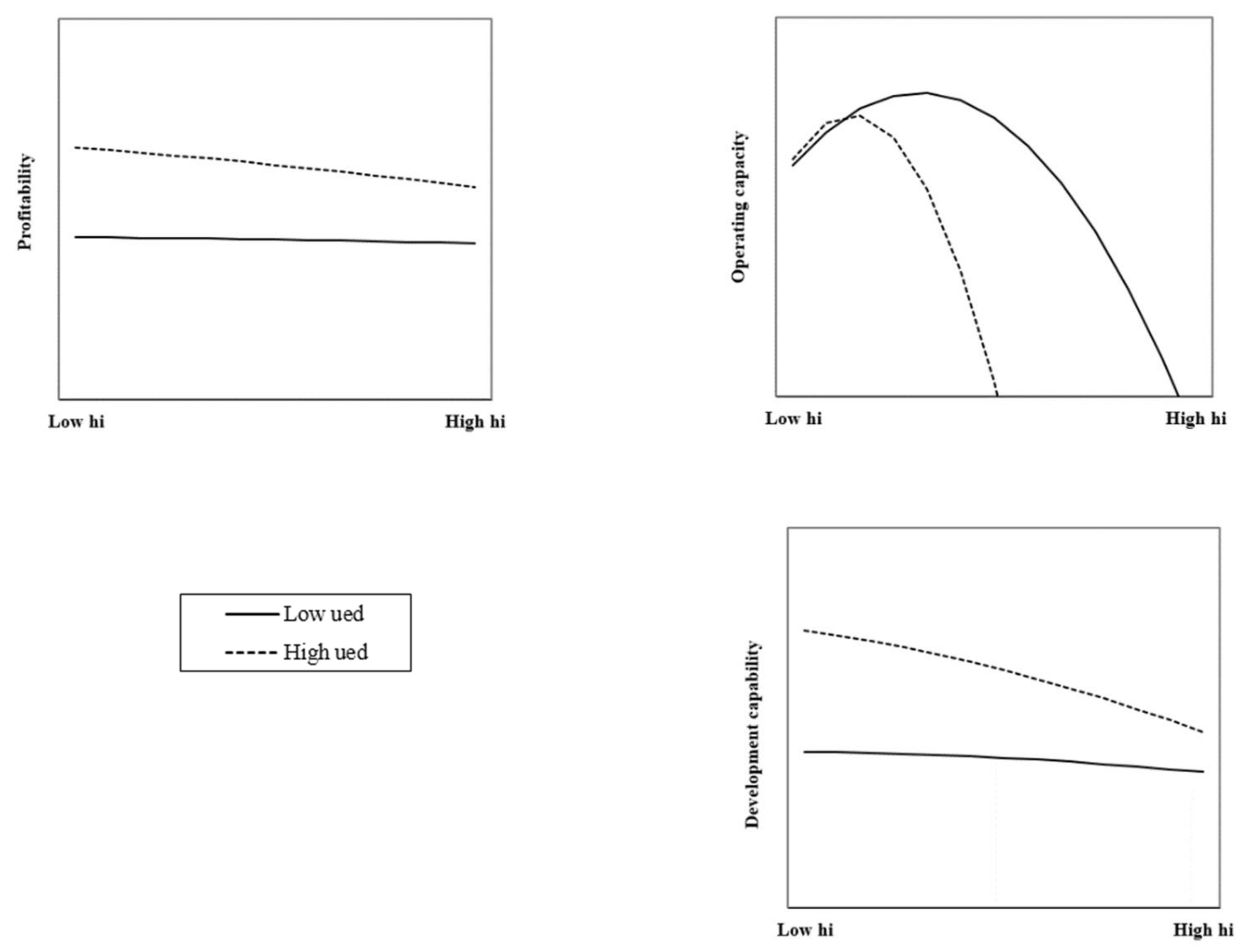

4.2. Analysis of Regression Results

4.3. Robustness Test

5. Conclusions and Discussion

5.1. Main Conclusions and Policy Implications

5.2. Limitations and Discussions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Model 1 | Model 2 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| roa | roe | tat | et | sgr | roa | roe | tat | et | sgr | |

| hi | −0.002 | −0.007 | 0.521 *** | 0.949 *** | −0.016 | −0.006 | −0.016 | 0.609 *** | 1.046 *** | −0.020 |

| (−0.20) | (−0.46) | (4.47) | (4.55) | (−0.86) | (−0.56) | (−0.86) | (4.77) | (4.67) | (−0.96) | |

| hi2 | −0.102 *** | −0.189 *** | −1.366 *** | −3.247 *** | −0.231 *** | −0.085 *** | −0.164 *** | −1.273 *** | −3.051 *** | −0.209 *** |

| (−3.66) | (−3.51) | (−3.66) | (−4.04) | (−4.00) | (−2.73) | (−2.90) | (−3.30) | (−3.67) | (−3.68) | |

| L.ued | 0.251 *** | 0.422 *** | 0.807 | 2.685 ** | 0.392 *** | |||||

| (4.30) | (3.73) | (1.28) | (2.28) | (3.41) | ||||||

| hi * L.ued | −0.908 *** | −1.436 *** | −5.429 ** | −12.360 ** | −1.345 *** | |||||

| (−3.13) | (−2.84) | (−1.98) | (−2.43) | (−3.12) | ||||||

| hi2 * L.ued | −3.087 ** | −4.745 ** | −32.088 *** | −63.258 *** | −5.177 ** | |||||

| (−2.44) | (−2.07) | (−2.85) | (−3.09) | (−2.22) | ||||||

| year | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Control variables | Control | Control | Control | Control | Control | Control | Control | Control | Control | Control |

| Constant term | −0.033 | −0.132 | 1.197 ** | 2.707 ** | −0.050 | −0.084 | −0.205 | 0.595 | 1.645 | −0.125 |

| (−0.61) | (−1.37) | (2.04) | (2.34) | (−0.55) | (−1.17) | (−1.58) | (0.92) | (1.23) | (−1.18) | |

| Observed value | 145 | 145 | 145 | 145 | 145 | 145 | 145 | 145 | 145 | 145 |

| Adjusted R2 | 0.442 | 0.299 | 0.336 | 0.409 | 0.306 | 0.480 | 0.320 | 0.275 | 0.353 | 0.297 |

| F-value | 13.90 *** | 5.799 *** | 3.084 *** | 3.311 *** | 3.664 *** | 14.17 *** | 6.750 *** | 2.886 *** | 2.830 *** | 4.781 *** |

| Variable | Model 1 | Model 2 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| roa | roe | tat | et | sgr | roa | roe | tat | et | sgr | |

| L.hi | −0.002 | −0.004 | 0.386 *** | 0.609 *** | 0.009 | −0.012 | −0.016 | 0.437 *** | 0.691 *** | 0.002 |

| (0.007) | (0.014) | (0.071) | (0.143) | (0.014) | (0.009) | (0.016) | (0.072) | (0.147) | (0.015) | |

| L.hi2 | −0.088 *** | −0.156 *** | −0.701 *** | −1.270 *** | −0.178 *** | −0.076 *** | −0.167 *** | −0.794 *** | −1.339 *** | −0.171 *** |

| (0.025) | (0.049) | (0.227) | (0.453) | (0.052) | (0.028) | (0.054) | (0.226) | (0.474) | (0.054) | |

| L.ued | 0.239 *** | 0.410 *** | 0.799 * | 1.634 * | 0.331 *** | |||||

| (0.053) | (0.103) | (0.466) | (0.954) | (0.096) | ||||||

| L.hi * L.ued | −0.577 *** | −0.681 * | −0.964 | −3.553 | −0.648 * | |||||

| (0.224) | (0.399) | (1.826) | (3.676) | (0.343) | ||||||

| L.hi2 * L.ued | −1.485 | −2.283 | −23.690 *** | −41.870 ** | −2.670 | |||||

| (0.957) | (1.941) | (9.061) | (18.427) | (1.925) | ||||||

| Control variables | Control | Control | Control | Control | Control | Control | Control | Control | Control | Control |

| Constant term | −0.064 | −0.157 * | 0.445 | 0.546 | −0.093 | −0.089 | −0.110 | 0.490 | 0.400 | −0.075 |

| (0.045) | (0.083) | (0.404) | (0.846) | (0.078) | (0.056) | (0.103) | (0.456) | (0.974) | (0.096) | |

| Wald chi2 | 215.90 | 78.85 | 43.64 | 42.83 | 54.44 | 246.27 | 117.02 | 66.50 | 56.21 | 78.26 |

| Observed value | 126 | 126 | 126 | 126 | 126 | 126 | 126 | 126 | 126 | 126 |

References

- Feng, F.; Chen, L.; Huang, H. The measurement and improvement path of the operational efficiency of Chinese port listed companies—Based on the SBM-DEA model. China Circ. Econ. 2017, 31, 106–112. [Google Scholar] [CrossRef]

- Xu, W.; Xu, Y. Comprehensive strength evaluation of coastal ports in my country and the evolution of the hinterland space of major ports. Econ. Geogr. 2018, 38, 26–35. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JJDL201805004&DbName=DKFX2018 (accessed on 22 March 2022).

- Clark, X.; Dollar, D.; Micco, A. Port efficiency, maritime transport costs, and bilateral trade. J. Dev. Econ. 2004, 75, 417–450. [Google Scholar] [CrossRef] [Green Version]

- Danielis, R.; Gregori, T. An input-output-based methodology to estimate the economic role of a port: The case of the port system of the Friuli Venezia Giulia Region, Italy. Marit. Econ. Logist. 2013, 15, 222–255. [Google Scholar] [CrossRef] [Green Version]

- Guerrero, D. Impacts of transport connections on port hinterlands. Reg. Stud. 2019, 53, 540–549. [Google Scholar] [CrossRef] [Green Version]

- Wang, Z.; Subramanian, N.; Abdulrahman, M.D.; Cui, H.; Wu, L.; Liu, C. Port sustainable services innovation: Ningbo port users’ expectation. Sustain. Prod. Consump. 2017, 11, 58–67. [Google Scholar] [CrossRef]

- Tongzon, J.L. Determinants of port performance and efficiency. Transp. Res. A 1995, 29, 245–252. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Farjoun, M. The independent and joint effects of the skill and physical bases of relatedness in diversification. Strateg. Manag. J. 1998, 19, 611–630. [Google Scholar] [CrossRef]

- Peng, M.W. Institutional transitions and strategic choices. Acad. Manag. Rev. 2003, 28, 275–296. [Google Scholar] [CrossRef] [Green Version]

- Khanna, T.; Palepu, K. Why focused strategies may be wrong for emerging markets. Harv. Bus. Rev. 1997, 75, 41–51. Available online: https://hbr.org/1997/07/why-focused-strategies-may-be-wrong-for-emerging-markets (accessed on 22 March 2022).

- Levy, H.; Sarnat, M. Diversification, portfolio analysis and the uneasy case for conglomerate mergers. J. Financ. 1970, 25, 795–802. [Google Scholar] [CrossRef]

- Franco, F.; Urcan, O.; Vasvari, F. Corporate diversification and the cost of debt: The role of segment disclosures. Account. Rev. 2016, 91, 1139–1165. [Google Scholar] [CrossRef]

- Stein, J.C. Internal capital markets and the competition for corporate resources. J. Financ. 1997, 52, 111–133. [Google Scholar] [CrossRef]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firm have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Teece, D.J. Economies of scope and the scope of the enterprise. J. Econ. Behav. Organ. 1980, 1, 223–247. [Google Scholar] [CrossRef]

- Scott, J. Multimarket contact and economic performance. Rev. Econ. Stat. 1982, 64, 368–375. [Google Scholar] [CrossRef]

- Rajan, R.; Servaes, H.; Zingales, L. The cost of diversity: The diversification discount and inefficient investment. J. Financ. 2000, 55, 35–80. [Google Scholar] [CrossRef] [Green Version]

- Myerson, R.B. Optimal coordination, mechanisms in generalized principle-agent problems. J. Math. Econ. 1982, 10, 67–81. [Google Scholar] [CrossRef]

- Harris, M.; Kriebel, C.H.; Raviv, A. Asymmetric information, incentives and intrafirm resource allocation. Manag. Sci. 1986, 28, 589–715. [Google Scholar] [CrossRef]

- Comment, R.; Jarrell, G.A. Corporate focus and stock returns. J. Financ. Econ. 1995, 37, 67–87. [Google Scholar] [CrossRef]

- Zhu, J. Diversified strategies and operating performance of listed companies in my country. Econ. Res. 1999, 11, 54–61. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JJYJ199911006&DbName=CJFQ1999 (accessed on 22 March 2022).

- Berger, P.G.; Ofek, E. Diversification’s effect on firm value. J. Financ. Econ. 1995, 37, 39–65. [Google Scholar] [CrossRef]

- Hoechle, D.; Schmid, M.; Walter, I.; Yermack, D. How much of the diversification discount can be explained by poor corporate governance? J. Financ. Econ. 2012, 103, 41–60. [Google Scholar] [CrossRef] [Green Version]

- Fuente, G.D.L.; Velasco, P. Capital structure and corporate diversification: Is debt a panacea for the diversification discount? J. Bank. Financ. 2020, 111, 105–122. [Google Scholar] [CrossRef]

- Hadlock, C.J.; Ryngaert, M.D.; Thomas, S. Corporate structure and equity offerings: Are there benefits to diversification? J. Bus. 2001, 74, 613–635. [Google Scholar] [CrossRef]

- Villalonga, B. Diversification discount or premium? new evidence from the business information tracking series. J. Financ. 2004, 59, 479–506. [Google Scholar] [CrossRef]

- Borda, A.; Geleilate, J.G.; Newburry, W.; Kundu, S.K. Firm internationalization, business group diversification and firm performance: The case of Latin American firms. J. Bus. Res. 2017, 72, 104–113. [Google Scholar] [CrossRef]

- Palich, L.E.; Cardinal, L.B.; Miller, C.C. Curvilinearity in the diversification-performance linkage: An examination of over three decades of research. Strateg. Manag. J. 2000, 21, 155–174. [Google Scholar] [CrossRef]

- Andreou, P.C.; Louca, C.; Petrou, A.P. Organizational learning and corporate diversification performance. J. Bus. Res. 2016, 69, 3270–3284. [Google Scholar] [CrossRef] [Green Version]

- Wang, Y.; Li, Z.; Zhang, B. The relationship between regional diversification and corporate performance—Based on the data of Chinese manufacturing listed companies. Econ. Probl. 2019, 5, 75–82. [Google Scholar] [CrossRef]

- Si, Z. Interactive development of port infrastructure and port city economy. Manag. Rev. 2015, 27, 33–43. [Google Scholar] [CrossRef]

- Zhao, Q.; Xu, H.; Wall, R.S.; Stavropoulos, S. Building a bridge between port and city: Improving the urban competitiveness of port cities. J. Transp. Geogr. 2017, 59, 120–133. [Google Scholar] [CrossRef]

- Cong, L.; Zhang, D.; Wang, M.; Xu, H.; Li, L. The role of ports in the economic development of port cities: Panel evidence from China. Transp. Policy 2020, 90, 13–21. [Google Scholar] [CrossRef]

- Guo, J.; Du, X.; Sun, C.; Wang, Z. Dynamic measurement and driving model of the relationship between ports and cities in the Bohai Rim. Geogr. Res. 2015, 34, 740–750. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?FileName=DLYJ201504013&DbName=CJFQ2015 (accessed on 22 March 2022).

- Guo, J.; Qin, Y.; Du, X.; Han, Z. Dynamic measurements and mechanisms of coastal port–city relationships based on the DCI model: Empirical evidence from China. Cities 2020, 96, 102–115. [Google Scholar] [CrossRef]

- Akhavan, M. Development dynamics of port-cities interface in the Arab Middle Eastern world—The case of Dubai global hub port-city. Cities 2017, 60, 343–352. [Google Scholar] [CrossRef]

- Boulos, J. Sustainable Development of Coastal Cities-Proposal of a Modelling Framework to Achieve Sustainable City-Port Connectivity. Procedia-Soc. Behav. Sci. 2016, 216, 974–985. [Google Scholar] [CrossRef] [Green Version]

- Xiao, Z.; Lam, J.S.L. A systems framework for the sustainable development of a Port City: A case study of Singapore’s policies. Res. Transp. Bus. Manag. 2017, 22, 255–262. [Google Scholar] [CrossRef]

- Zhao, Y.; Zhou, J.; Zhong, Y.; Chi, G. Research on the development mechanism of green growth in port cities—Dual mechanism based on growth synergy and resource constraints. Manag. Rev. 2018, 30, 46–59. [Google Scholar] [CrossRef]

- Lu, B.; Xing, J.; Wang, Q.; Wang, S. Panel data analysis of port competitiveness and hinterland economic coordination mechanism. Syst. Eng.-Theory Prac. 2019, 39, 1079–1090. [Google Scholar] [CrossRef]

- Lu, B.; Qiu, W.; Xing, J.; Wen, Y. Research on the development strategy of China’s coastal nodes and ports based on the “Belt and Road” initiative. Syst. Eng.-Theory Prac. 2020, 40, 1627–1639. [Google Scholar] [CrossRef]

- Berry, C.H. Corporate growth and diversification. J. Law Econ. 1971, 14, 371–383. [Google Scholar] [CrossRef]

- Aivazian, V.A.; Rahaman, M.M.; Zhou, S. Does corporate diversification provide insurance against economic disruptions? J. Bus. Res. 2019, 100, 218–233. [Google Scholar] [CrossRef]

- Jacquemin, A.P.; Berry, C.H. Entropy measure of diversification and corporate growth. J. Indust. Econ. 1979, 27, 359–369. [Google Scholar] [CrossRef]

- Raghunathan, S.P. A refinement of the entropy measure of firm diversification: Toward definitional and computational accuracy. J. Manag. 1995, 21, 989–1002. [Google Scholar] [CrossRef]

- Zeng, P.; Liao, M.; Wang, J. Regional diversification or product diversification? Private enterprise core competence construction and growth strategy selection under the constraints of institutional environment. Manag. Rev. 2020, 32, 197–210. [Google Scholar] [CrossRef]

- Wei, M.; Li, S. A Study on the Measurement of the High-Quality Development Level of China’s Economy in the New Era. Quant. Econ. Technical Econ. Res. 2018, 35, 3–20. [Google Scholar] [CrossRef]

- Xie, C.; Zhong, Z. Application of entropy weight method in comprehensive evaluation of bank’s operating performance. China Soft Sci. 2002, 9, 108–111. Available online: http://kns.cnki.net/kcms/detail/detail.aspx?FileName=ZGRK200209022&DbName=CJFQ2002 (accessed on 22 March 2022).

- Wen, Z.; Hou, J.; Zhang, L. Comparison and application of regulatory effect and intermediary effect. Psychol. J. 2005, 2, 268–274. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?FileName=XLXB20050200F&DbName=CJFQ2005 (accessed on 22 March 2022).

- Fang, J.; Wen, Z.; Liang, D.; Li, N. Analysis of moderating effects based on multiple regression. Psychol. Sci. 2015, 38, 715–720. [Google Scholar] [CrossRef]

- Hua, C.; Chen, J.; Wan, Z.; Xu, L.; Bai, Y.; Zheng, T.; Fei, Y. Evaluation and governance of green development practice of port: A sea port case of China. J. Clean Prod. 2020, 249, 119434. [Google Scholar] [CrossRef]

- Wang, L.; Chen, Y.; Ramsey, T.S.; Hewings, G.J.D. Will researching digital technology really empower green development? Technol. Soc. 2021, 66, 101–113. [Google Scholar] [CrossRef]

- Jiang, B.; Haider, J.; Li, J.; Wang, Y.; Yip, T.L.; Wang, Y. Exploring the impact of port-centric information integration on port performance: The case of Qingdao Port. Marit. Policy Manag. 2021, 48, 1–26. [Google Scholar] [CrossRef]

| Target Layer | Criterion Layer | Indicator Layer | X | |

|---|---|---|---|---|

| Indicator | Unit | |||

| UED level | Economic scale | Regional GDP | 100 million RMB | X1 |

| Total social investments in fixed assets | 100 million RMB | X2 | ||

| Benefit level | GDP per capita | RMB | X3 | |

| Average wage of employees | RMB | X4 | ||

| Economic structure | Proportion of the secondary industry’s output value | % | X5 | |

| Proportion of the tertiary industry’s output value | % | X6 | ||

| Degree of opening up | Total value of imports and exports | 100 million USD | X7 | |

| Actual amount of foreign capital utilized | 100 million USD | X8 | ||

| Type of Variable | Name of Variable | Symbol | Definition |

|---|---|---|---|

| Dependent | Return on total assets | roa | Net profit/Average total assets × 100% |

| Return on net assets | roe | Net profit/Average total shareholders’ equity × 100% | |

| Turnover of total assets | tat | Net operating income/Average total assets | |

| Turnover of net assets | et | Net operating income/Average shareholders’ equity | |

| Sustainable growth rate | sgr | Return on net assets × Earnings retention rate/(1 − Return on net assets × Earnings retention rate) | |

| Independent | HI | hi | 1 − ∑(proportion of each segment’s sales revenue to the enterprise’s total sales revenue)2 |

| Regulatory | UED | ued | ∑(Various economic evaluation indicators × Weight from entropy calculation) |

| Control | Enterprise size | asset | Expressed by the natural logarithm of the total assets at end of period: ln(ASSET) |

| Asset–liability ratio | lev | Total liabilities/Total assets × 100% | |

| Ratio of shares held by the largest shareholder | share | Number of shares held by the largest shareholder/Total number of shares held by the listed enterprise | |

| Years of establishment | age | Expressed by the logarithm of the years of enterprise’s establishment: ln(AGE + 1) | |

| Year effect | year | Sampling years for the enterprises were 2012–2019. A total of 8 years and 7 dummy variables were included |

| Variable | Observed Value | Mean | Standard Deviation | Minimum Value | Maximum Value |

|---|---|---|---|---|---|

| roa | 145 | 0.045 | 0.026 | 0.001 | 0.100 |

| roe | 145 | 0.076 | 0.043 | 0.001 | 0.177 |

| tat | 145 | 0.349 | 0.325 | 0.003 | 1.772 |

| et | 145 | 0.660 | 0.731 | 0.0429 | 5.300 |

| sgr | 145 | 0.062 | 0.045 | −0.020 | 0.228 |

| hi | 145 | 0.385 | 0.237 | 0 | 0.830 |

| ued | 145 | 0.059 | 0.048 | 0.003 | 0.176 |

| lnasset | 145 | 23.440 | 1.017 | 20.770 | 25.780 |

| lev | 145 | 0.409 | 0.111 | 0.075 | 0.722 |

| share | 145 | 0.517 | 0.165 | 0.154 | 0.795 |

| age | 145 | 2.745 | 0.488 | 0.693 | 3.466 |

| Test | Statistics | p Value |

|---|---|---|

| LM test | chibar2 = 128.66 | 0.0000 |

| F test | F = 10.50 | 0.0000 |

| Hausman test | chi2 = 4.29 | 0.9935 |

| Variable | roa | roe | tat | et | sgr | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 1 | Model 2 | Model 1 | Model 2 | Model 1 | Model 2 | Model 1 | Model 2 | |

| hi | −0.009 | −0.015 * | −0.023 * | −0.032 ** | 0.367 *** | 0.419 *** | 0.521 *** | 0.607 *** | −0.022 * | −0.029 ** |

| (0.007) | (0.008) | (0.013) | (0.014) | (0.065) | (0.068) | (0.139) | (0.153) | (0.012) | (0.013) | |

| hi2 | −0.082 *** | −0.059 ** | −0.158 *** | −0.145 *** | −0.982 *** | −1.026 *** | −1.642 *** | −1.741 *** | −0.211 *** | −0.211 *** |

| (0.024) | (0.025) | (0.044) | (0.049) | (0.212) | (0.208) | (0.476) | (0.496) | (0.044) | (0.046) | |

| L.ued | 0.254 *** | 0.436 *** | 0.778 * | 1.831 * | 0.339 *** | |||||

| (0.052) | (0.099) | (0.450) | (0.950) | (0.095) | ||||||

| hi * L.ued | −0.734 *** | −0.859 ** | −1.097 | −3.664 | −0.596 * | |||||

| (0.210) | (0.382) | (1.723) | (3.814) | (0.330) | ||||||

| hi2 * L.ued | −2.098 ** | −3.035 | −22.165 ** | −44.071 ** | −2.826 | |||||

| (0.943) | (1.889) | (8.821) | (19.045) | (1.834) | ||||||

| lnasset | 0.009 *** | 0.010 *** | 0.015 *** | 0.014 *** | −0.034 ** | −0.034 ** | −0.051 | −0.047 | 0.009 *** | 0.008 ** |

| (0.002) | (0.002) | (0.003) | (0.003) | (0.016) | (0.016) | (0.037) | (0.041) | (0.003) | (0.003) | |

| lev | −0.119 *** | −0.071 *** | −0.053 ** | 0.006 | 0.039 | 0.133 | 1.151 *** | 1.407 *** | −0.002 | 0.062 ** |

| (0.013) | (0.016) | (0.024) | (0.032) | (0.137) | (0.139) | (0.292) | (0.311) | (0.025) | (0.031) | |

| share | −0.005 | −0.009 | −0.001 | −0.009 | 0.282 *** | 0.221 ** | 0.466 ** | 0.385 * | 0.046 ** | 0.029 |

| (0.011) | (0.011) | (0.020) | (0.021) | (0.090) | (0.094) | (0.198) | (0.209) | (0.019) | (0.020) | |

| age | −0.006 * | −0.011 *** | −0.014 ** | −0.027 *** | 0.159 *** | 0.149 *** | 0.182 *** | 0.200 *** | −0.011 | −0.028 *** |

| (0.004) | (0.004) | (0.007) | (0.008) | (0.037) | (0.039) | (0.068) | (0.077) | (0.008) | (0.009) | |

| year | yes | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Constant term | −0.077 * | −0.114 ** | −0.181 ** | −0.168 * | 0.461 | 0.445 | 0.448 | 0.205 | −0.129 * | −0.079 |

| (0.041) | (0.048) | (0.073) | (0.091) | (0.374) | (0.409) | (0.877) | (1.015) | (0.072) | (0.086) | |

| Wald chi2 | 224.04 | 274.87 | 91.62 | 121.42 | 52.00 | 83.38 | 38.92 | 55.63 | 59.03 | 77.44 |

| Observed value | 145 | 145 | 145 | 145 | 145 | 145 | 145 | 145 | 145 | 145 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sun, Y.; Zhang, S.; Wu, S. Impact of Ports’ Diversification-Driven Industrial Transformation on Operating Performance: Regulatory Effect of Port Cities’ Urban Economic Development Level. Water 2022, 14, 1243. https://doi.org/10.3390/w14081243

Sun Y, Zhang S, Wu S. Impact of Ports’ Diversification-Driven Industrial Transformation on Operating Performance: Regulatory Effect of Port Cities’ Urban Economic Development Level. Water. 2022; 14(8):1243. https://doi.org/10.3390/w14081243

Chicago/Turabian StyleSun, Yanfang, Shuhui Zhang, and Shuang Wu. 2022. "Impact of Ports’ Diversification-Driven Industrial Transformation on Operating Performance: Regulatory Effect of Port Cities’ Urban Economic Development Level" Water 14, no. 8: 1243. https://doi.org/10.3390/w14081243