A Study on the Mechanism and Pricing of Drainage Rights Trading Based on the Bilateral Call Auction Model and Wealth Utility Function

Institute of Environmental Accounting and Asset Management, Hohai University, Nanjing 211100, China

*

Author to whom correspondence should be addressed.

Water 2022, 14(14), 2269; https://doi.org/10.3390/w14142269

Submission received: 12 June 2022

/

Revised: 15 July 2022

/

Accepted: 18 July 2022

/

Published: 21 July 2022

(This article belongs to the Section Water Resources Management, Policy and Governance)

Abstract

:In the context of the high incidence of flooding disputes among neighboring subjects in the basin, exploring the drainage rights trading mechanism and clarifying the pricing method of drainage rights are new ideas to manage flooding disasters. In this study, the trading mechanism of drainage rights is constructed using a bilateral call auction model, in which the price constraint, the control total quantity constraint, the clearing rule, and the matching rule are explained. In addition, we adopt the wealth utility concept to construct a function, apply the social welfare function to associate the wealth utility functions of both sides of the transaction, and draw on the environmental Gini coefficient concept to construct a pricing model for drainage rights transactions based on fairness and efficiency. Finally, we conduct an arithmetic simulation of the drainage rights trading mechanism and transaction pricing for China’s Jiangsu section of the Huaihe River Basin. The study’s results show that the trading mechanism model can give the optimal trading scheme when multiple subjects are trading drainage rights. This fills the gap in existing studies and can lead to efficient trading of drainage rights. At the same time, the pricing model can give the optimal transaction price that considers efficiency and fairness, providing a more practical pricing theory for drainage rights trading.

1. Introduction

Flood security is an essential part of national security [1,2,3]. However, the established economic and social pattern and basic national conditions of China are that the population and economic factors are concentrated in the high-risk areas of flooding at the tail of rivers, and losses from floods and droughts account for about 70% of losses from all types of natural disasters [4], so studies related to flood exclusion have been highly valued. Drainage rights management has received more widespread attention as a non-engineering tool to rationalize the planning of each region’s drainage authority from the perspective of economic and resource management. Drainage rights are the authority of a subject (e.g., a province or municipality) to remove flood water into a river. Drainage rights can generally be acquired in two ways: by accepting an allocation from a higher level of government (initial allocation of drainage rights) and purchasing drainage rights from other parties (trading of drainage rights). Drainage rights trading is a transaction that relies on the difference in the economic level of neighboring regions to drain flood water from the economically strong to the economically weak. Since the transaction price is between the flood losses of both trading parties, the transaction will not only make both trading parties profit from it but also lower the overall flood losses of the region.

The concept of drainage rights was proposed in 2014 [5]. At present, the research perspectives of drainage rights mainly contain the necessity and feasibility of initial and reallocation, the control total and allocation mechanism of initial allocation, the trading mechanism of drainage rights, and the pricing of trading [6,7,8,9,10,11,12,13]. The research in this paper focuses on the trading mechanism and pricing of drainage rights. Concerning the trading mechanism of drainage rights, Chinese scholars have used the evolutionary game model to design the operating mechanism of drainage rights trading under “quasi-market” conditions [14]. Scholars in other countries have conducted more case studies, such as flood risk transfer mechanisms in the UK, flood-resilient discharge mechanisms in the Netherlands, and rainwater storage projects in Japanese cities, among others [15,16,17,18]. In general, the existing research is relatively poor and fragmented. In addition, these studies all contain a research assumption that the number of buyers and sellers is one. The high incidence of drainage rights trading is a time of flooding, and it is common for multiple entities to need to buy or sell drainage rights at the same time. Therefore, broadening the perspective of research in this area is needed. In terms of pricing the transactions of drainage rights, Chinese scholars have used methods containing the entire cost method, flood loss assessment method, and asymmetric information bargaining model [19,20]. Studies by scholars in other countries still focus on case studies, such as the drainage charging system in the UK and the “stormwater fee” system in Germany [21,22,23,24,25]. In general, the underlying philosophy of these studies remains the use of flood losses as a lower bound on the price of trading drainage rights, which is certainly very reasonable. However, the construction of an asymmetric information bargaining model has triggered scholars to think about it. We should not only focus on the actual cost of the drainage rights but also on the profit game between the two sides of the drainage rights transaction [26]. The asymmetric information bargaining model only gives the game process of drainage rights trading and cannot tell us the optimal trading price after the game.

To overcome the shortcomings of the above study, we explore the optimal matching scheme of transaction subjects when there are multiple sellers and buyers. To this end, we apply the bilateral call auction model to construct a trading mechanism for drainage rights, in which the price constraint, the control total constraint, the clearing rule, and the matching rule are explained. Bilateral call auction models have been applied to pricing wastewater discharge rights, water rights, and electricity [27,28]. It can give an optimal trading scheme when multiple subjects participate in the transaction. Thus, the method applies to the study of drainage rights trading mechanisms. In addition, we adopt the wealth utility concept to construct a function, apply the social welfare function to associate the wealth utility functions of both sides of the transaction, and draw on the environmental Gini coefficient concept to construct a pricing model for drainage rights transactions based on parallel equity and efficiency. The wealth utility function has been applied to financial products and the pricing of wastewater discharge rights, among others [29], and its intrinsic idea is to focus on the satisfaction of buyers and sellers for profits. Thus, we introduce it as a new idea for pricing drainage rights. Finally, we conducted an arithmetic simulation of the drainage rights trading mechanism and transaction pricing for China’s Jiangsu section of the Huaihe River Basin. In summary, the article’s innovation lies first in applying the bilateral call auction model and the wealth utility function. The above two models better solve the subject matching and pricing problems of drainage rights trading. Second, we set the “unfair pullback coefficient” in the pricing model, which significantly improves the fairness of the pricing of drainage rights. Finally, we derive the optimal trading price instead of discussing only the effect of the model’s parameters on the optimal trading price. This provides a more practical pricing theory for drainage rights trading.

2. Study on the Transaction Mechanism of Bilateral Call Auction of Drainage Rights

2.1. Basic Assumptions

Assumption 1.

There are multiple potential buyers of drainage rights Bi and sellers Sj in a given area. Bi denotes the ith drainage right purchaser in the region, Sj denotes the jth drainage right seller in the region, m denotes the number of purchasers, and n denotes the number of sellers. Generally, a subject unit tends to be a seller of drainage rights when its flood losses are low or when the drainage power generates a surplus, and conversely tends to be a purchaser [7].

Assumption 2.

Set the unit flood loss values for the ith drainage right purchaser and the jth drainage right seller as Cbi and Csj. Unit flood economic loss is abbreviated as unit flood loss (hereinafter), which indicates the direct economic loss formed by a unit of flooding suffered by a trading entity. The unit flood loss is closely related to the economic level of the region [30].

Assumption 3.

Set the transaction demand of the ith drainage right buyer and the jth drainage right seller as xi and yj, and the expected transaction prices as oi and fj. xi and yj reflect the difference between the total demand for flood discharge of the subject and the number of drainage rights received in the initial allocation; oi reflects the ith drainage right purchaser’s assessment of the value of the drainage rights existing in the market (let the ith drainage right purchaser consider the lowest value of the drainage rights existing in the market to be fmin), and oi is less than or equal to the unit flood loss (Cbi) of the ith drainage right purchaser, then we have fmin ≤ 2264oi ≤ Cbi; fj should be greater than or equal to the unit flood loss of the jth drainage rights seller (Csj) in the case of non-power surplus out of rational economic man assumption, i.e., fj ≥ Csj.

Assumption 4.

Set the expected benefits in the transaction between the ith drainage right buyer Bi and the jth drainage right seller Sj as Wi (Cbi) and Uj (Csj). The revenue expected by the buyer and seller of drainage rights in a transaction can be understood as the product of the expected unit profit and the expected number of transactions. In this study, the expected unit profit of the drainage rights purchaser in the transaction is the difference between the flood losses that the purchaser can avoid through the transaction and the expected purchase price, i.e., Cbi-oi; The expected unit profit of the seller of drainage rights in a transaction is the difference between the seller’s expected sales price and the additional flood losses sustained as a result of the transaction, i.e., fj-Csj; Then Wi (Cbi) = xi ∗ (Cbi − oi) and Uj (Csj) = yj ∗ (fj − Csj).

2.2. Model Construction

From Assumptions 3 and 4, it can be seen that when oi ≥ fj, both parties to the transaction have the expected profit margin and are satisfied with each other’s offers, and the transaction holds, at which time the equilibrium price P0 = (oi + fj)/2. When oi < fj, the seller fails to obtain the entire expected profit margin, and the transaction does not hold. In the state of incomplete information, multiple solutions of Bayesian Nash equilibrium exist, requiring the design of trading rules and trading systems for bilateral call auctions, in which we consider that market participants expect to maximize not only their returns in centralized bidding but also the social returns. Expressing the above expectations in the functional form will result in the following objective function.

2.2.1. Rational Price Constraints

After understanding the expectations of the objective function, we give the constraints on the objective function. The construction of the bilateral call auction model is based on the rational economic man’s assumption that rational risk brokers decide to trade and have non-negative returns [31]. This leads to Equations (3) and (4).

2.2.2. Macroscopic Control Total Quantity Constraints

Drainage rights trading is a secondary adjustment to the initial allocation of drainage rights that have been implemented by the higher level of government, and the initial and secondary allocations reflect the joint role of administrative and market instruments for the allocation of resources (disasters) [9]. The primary allocation forms a benchmark pattern for the discharge of flood water and the use of rivers. The secondary allocation is conducive to improving the problems of the initial allocation in which the amount of local allocation does not match the actual demand, and the marketization of drainage rights is conducive to promoting cross-regional water trade. However, excessive secondary adjustment can cause specific hazards, such as flooding that threatens the safety of people’s lives and property in local areas or economic speculation that leads to drainage rights trafficking [8,9,10]. Therefore, the higher government is committed to controlling the final situation of flood distribution by limiting the total number of drainage rights traded in a particular area as a macro-regulatory measure, as shown in Equation (5).

where Q is the maximum restricted transaction volume decided by the higher level of government, i.e., the drainage rights (if any) below the volume of Q will have the power to trade (note that here it is only the power to trade and does not indicate a successful trade). g and h are referred to as the number of buyers and sellers included in the trading set, respectively, and xi and yj denote the trading demand of the ith drainage right buyer and the jth drainage right seller, respectively.

2.3. Clearance Rules

Drainage rights bilateral call auction participants include higher government, water companies, the two sides of the transaction, and so on (ignoring possible tax collection subjects). The basic process is as follows: the two sides of the transaction on the purchase or sale of drainage rights to register (including basic information, expected transaction price, transaction demand, etc.), submitted to the relevant departments for application, after review, by intermediaries (usually water companies) to Bidding. The target transaction volume and the target transaction price quoted by both sides of the transaction respectively form the buyer’s offer set b* and the seller’s offer set s*, and the buyer’s offer set b* is arranged in descending order to get b* = {o1, o2, o3..., og,... om}, the set of seller’s offers s* is arranged in ascending order to get s* = {f1, f2, f3...,fh,... fn}, where o1 ≥ o2 ≥ o3 ≥ og ≥ om and f1 ≤ f2 ≤ f3 ≤ fh ≤ fn. Assuming fh ≤ og < fh+1 and og < fh ≤ og+1, the top g subjects in the buyer’s offer set and the top h subjects in the seller’s offer set enter the transaction set from the offer set, and this rule is called the clearing rule for bilateral call auctions [32]. At this point, we can write the transaction set of the buying side as B* = {B1, B2, B3..., Bg} and the transaction set of the selling side as S* = {S1, S2, S3..., Sh}.

2.4. Matching Rules

According to the priority order, the first B1 in the buyer’s transaction set will get the first choice, and its selection process is more complicated, with the main reference factors being the seller’s expected sales price, sales demand, related taxes and fees, political considerations, etc. Therefore, B1 does not necessarily consider only the lowest priced S1, so it brings the following picture: (1) B1 fails to choose S1 as counterparty, B2 still enjoys the option to trade with S1; (2) B1 chooses S1 as counterparty, but S1’s target trading volume does not fully satisfy B1’s demand, so B1 chooses another seller as second counterparty; (3) B1 chooses S1 as counterparty, but S1 still has spare volume for other purchasers to choose after trading with B1.

3. Transaction Pricing Study of Bilateral Call Auction for Drainage Rights

3.1. Wealth Utility Function Construction

From Assumption 3, the equilibrium price P0 = (oi + fj)/2 for the drainage rights transaction. The equilibrium price at this point is not affected by the parameters and is the transaction price in perfect equilibrium. The transaction price in perfect equilibrium can distribute the difference between the expected transaction prices of the two parties fairly in terms of quantity. However, the pricing of drainage rights transactions should not only take the equal distribution of proceeds between the buyer and the seller as the whole concept, but the satisfaction of both parties to the transaction with the proceeds received and the fairness of resource allocation should also be reflected [33]. Therefore, we adopt the wealth utility concept to construct the function, apply the social welfare function to associate the wealth utility functions of both sides of the transaction, and draw on the environmental Gini coefficient concept to construct a pricing model for drainage rights transactions based on parallel equity and efficiency.

Wealth utility indicates the degree of satisfaction of both parties to the transaction with the benefits obtained from the transaction [34], e.g., given the same volume of benefits for people at different Engel coefficient levels, it is clear that people with higher Engel coefficients receive a higher level of satisfaction. The utility space of the drainage rights transaction (called the “total utility space”) is the difference between the expected transaction prices of the two parties to the transaction, as can be derived from this study. The difference between the buyer’s expected transaction price and the actual transaction price can be called the “buyer’s utility space”, and the difference between the seller’s actual transaction price and its expected transaction price can be called the “seller’s utility space”, and their ratios to the total utility space can be called the “Degree of utility acquisition of the buyer” and the “Degree of utility acquisition of the seller”, respectively.

The wealth utility function construction of the buyer.

The wealth utility function construction of the seller.

In Equations (6) and (7), p* denotes the actual transaction price, which should be between the desired prices of the two sides of the transaction, i.e., fj ≤ p* ≤ oi; oi-p* denotes the utility space of the buyer, and p*-fj denotes the utility space of the seller, i.e., the buyer and seller split the total utility space oi-fj; Zb(p*) denotes the degree of utility acquisition of the buyer, and Zs(p*) denotes the degree of utility acquisition of the seller. When the actual transaction price exceeds the buyer’s expected purchase price, i.e., p* > oi, the buyer’s willingness to trade is 0. When the actual transaction price is less than the seller’s expected sales price, i.e., p* < fj, the seller’s willingness to trade is 0. Then in both cases, the transaction is not valid.

3.2. Social Welfare Function Construction

Social welfare is an important element in economics that aims to explore the goals pursued by society [35]. The social welfare function has experienced three expressions: additive, multiplicative, and minimalist. In this study, a two-person Nash multiplier-type social welfare function is selected to combine the utility functions of the two parties to the transaction [36], and the indicator “unfair pullback coefficient” is set according to the concept of environmental Gini coefficient [37]. A pricing model for drainage rights transactions based on equity and efficiency is constructed as follows.

where Zb(p*) denotes the degree of utility acquisition of the buyer, Zs(p*) denotes the degree of utility acquisition of the seller, T denotes the value of the social welfare function, and α denotes the inequity pullback coefficient. The unfair pullback coefficient reflects the loss of flooding carried per unit of a given indicator. Based on existing literature, we argue that such a flood distribution is equitable when the loss of flooding per unit of GDP, area, and population carried by two regions is close [38]. Thus, this study is based on the three dimensions of economic development level, land area, and population size to calculate the unfair pullback coefficient. Considering that the direct economic loss of flooding in the study year of the drainage rights seller may be zero, it will lead to the unfair pullback coefficient of the drainage rights buyer is 1, which loses the significance of the setting, so we chose to extend the data for three years. In summary, the inequitable pullback factor is calculated as follows.

where xae represents the arithmetic mean of the number of indicators in region e in the ath three previous years, yae represents the arithmetic mean of the direct economic losses from flooding in the ath region in the previous three years, and e represents the number of the three indicators: GDP, land area, and population.

3.3. Solving for the Transaction Price

In addition, a series of derivations from Equation (8) leads to a conclusion that the social welfare function T achieves its maximum value when , i.e., the formula for the optimal transaction price p* is derived. The derivation process is as follows. First, organize Equation (8) to derive ; second, find the derivative of the social welfare function T; third, extract the common factorization to obtain ; fourth, in order to find the extreme value point of the social welfare function T, so that the derivative function T’ is zero, i.e., , and because in general p* is not equal to oi and fj (the expected transaction price between the two sides of the transaction), there exists the equation , by which can be found; finally, as is a monotonically decreasing primary linear function, indicating that there is only one solution to the equation, and the original function first increases and then decreases, that is, to find the p* for the original function of the only extreme value point and the extreme value of the maximum.

4. Simulation of Calculations for Drainage Rights Trading in Jiangsu Section of Huaihe River Basin

4.1. Study Area

The Jiangsu section of the Huaihe River Basin, mainly flowing through the north-central region of Jiangsu Province, China, involves eight prefecture-level cities, namely Xuzhou, Nantong, Lianyungang, Huaian, Yancheng, Yangzhou, Taizhou and Suqian, located at 116°22′–121°00′ E and 32°23′–35°07′ N. It is the easternmost section of the Huaihe River Basin, connecting the Tong Yang Canal and the Yangtze River Basin to the south, reaching the Yiliu hilly mountains and the Yellow River Basin to the north, the Yimeng Mountains. There are many lakes and rivers in the Jiangsu section of the watershed, including Hongze Lake, the Beijing–Hangzhou Grand Canal, and the Huaishu New River, among which the Hongze Lake Wetland is an important freshwater wetland reserve in China with a good environment and a variety of biological and plant resources.

4.2. Simulation of Drainage Rights Trading Mechanism

At present, drainage rights trading has not yet entered the pilot phase. In this context, we performed numerical simulations based on existing research results (Buuren et al., 2016; Wang, H.-F. et al., 2014). Let there be eight participants in the drainage rights trading market in the Jiangsu section of the Huaihe River Basin at a specific moment, including four drainage rights buyers and four drainage rights sellers, and both parties make independent offers. The quoted and traded quantities on the buying side are B1(8.14, 100), B2(5.38, 50), B3(7.21, 100), and B4(5.2, 62.5), and the quoted and traded quantities on the selling side are S1(9.45, 100), S2(6.8, 75), S3(6.47, 50), and S4(4.38, 37.5), so the buying and selling total demand is 312.5 m3 and 262.5 m3 respectively. Let the total limit of drainage rights trading by the higher government be 250 m3, which indicates that there will be 62.5 m3 of total demand for drainage rights purchase and 12.5 m3 of total demand for drainage rights sale that cannot be satisfied.

4.2.1. Clearance Rule

According to the clearing rule, the set of buyers’ offers b* is arranged in descending order to get b* = {8.14, 7.21, 5.83, 5.20}, the set of sellers’ offers s* is arranged in ascending order to get s* = {4.38, 6.47, 6.80, 9.45}, and the final results are shown in Table 1. Since only 250 m3 of drainage rights are allowed to be traded, purchaser B4 will be strictly excluded from the transaction set, and the expected sales price f1 of seller S1 is greater than any value in the purchaser’s offer set b*, indicating that it is not possible to match and reach a deal with either purchaser. Therefore, we can write the transaction set for the buyer as B* = {B1, B3, B2} and the transaction set as S* = {S4, S3, S2}.

4.2.2. Matching Transaction Sets

First, in order of priority, B1 in the buyer’s transaction set will get the first choice, and its selection process is more complicated, with the main reference factors being the seller’s offer, the seller’s expected transaction volume, and relevant taxes, political considerations, etc. In this case, only the expected sales price of the seller and the expected transaction volume are used as reference factors. The consideration process is: (1) B1’s acquisition demand x1 = 100, which is a large amount, gives priority to the full drainage rights of seller S4 and considers the remaining 62.5 m3. However, the expected sales price of seller S3 is slightly smaller than the expected sales price of seller S4, but it does not fully satisfy B1’s remaining demand, and B1 tends to choose seller S2 for the 62.5 m3 transaction. (2) After all of B1’s acquisition demand is satisfied, B3 will be given the preference, and B3’s acquisition demand x3 = 100, which is also a large amount. At this time, the total expected sales volume remaining on the selling side is 62.5 m3 (50 m3 remaining on the selling side S3 and 12.5 m3 remaining on the selling side S2), then the purchasing side B3 will purchase the entire remaining volume of 62.5 m3. By observing Table 1, it can be found that the transaction demands of both drainage right buyer B2 and drainage right buyer B4 are not satisfied due to the low bids.

In summary, the final results are shown in Table 2, with a total transaction volume of 162.5 m3 (less than the total restricted amount of drainage rights trading), and four transactions were formed, as follows: (1) buyer B1 and seller S4 find the optimal transaction price between 4.38 RMB/m3 and 8.14 RMB/m3 for 37.5 m3 of flooding and reach a deal; (2) purchaser B1 and seller S2 find the optimal transaction price between 6.80 RMB/m3 and 8.14 RMB/m3 for 62.5 m3 of flood discharge and reach a deal; (3) purchaser B3 and seller S3 find the optimal transaction price between 6.47 RMB/m3 and 7.21 RMB/m3 for a 50 m3 flood discharge and reach a deal; (4) purchaser B3 and seller S2 find the optimal transaction price between 6.80 RMB/m3 and 7.21 RMB/m3 for a 12.5 m3 flood discharge and reach a deal. In the following, the optimal transaction price will be selected for these four transactions.

4.3. Simulation of the Pricing of Drainage Rights Transactions

The simulation of the pricing of the drainage rights transaction includes the construction of the wealth utility function, the construction of the welfare function, the unfair pullback coefficient solution, and the optimal transaction price solution. We only take the first transaction as an example for detailed analysis and explanation.

4.3.1. Wealth Utility Function

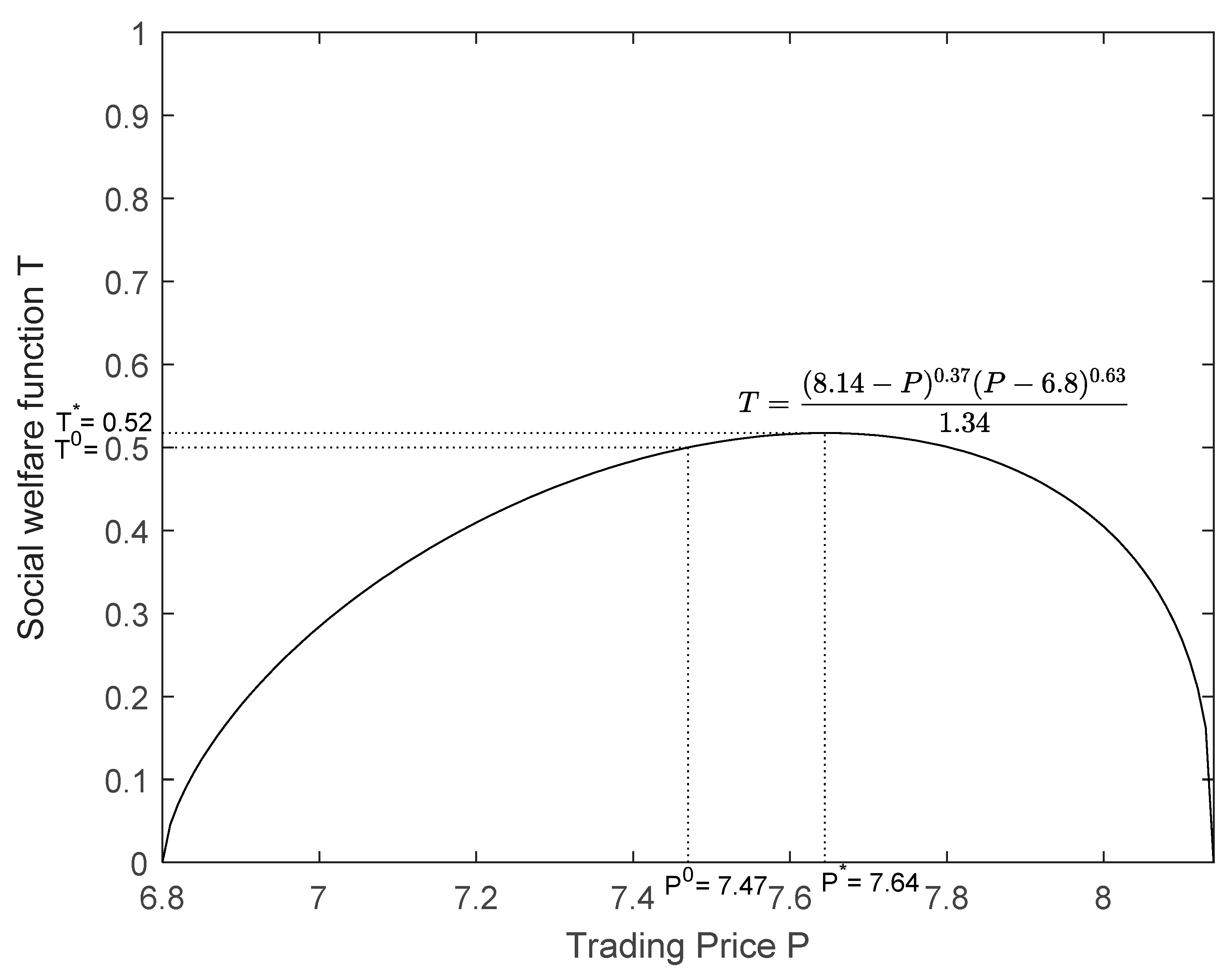

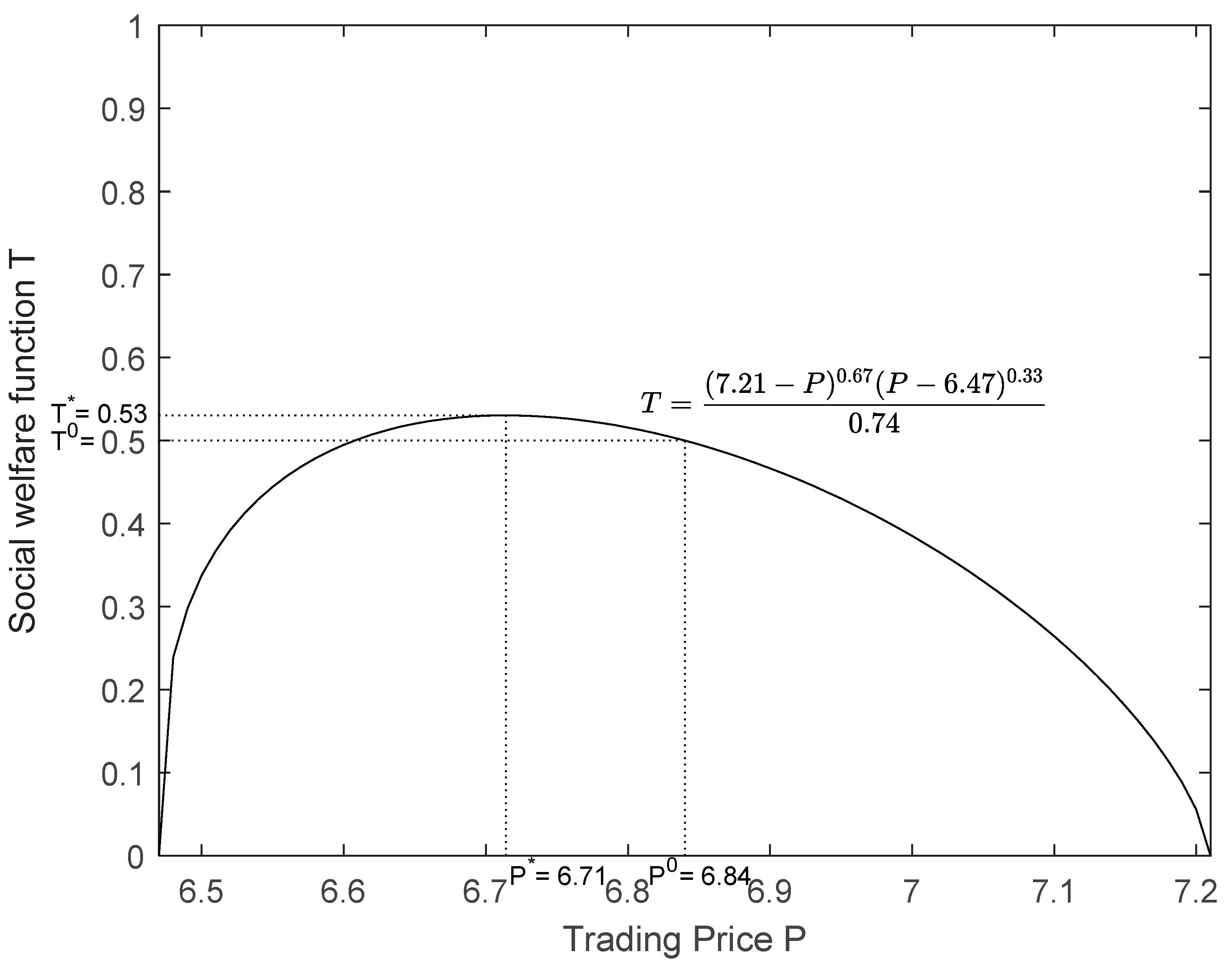

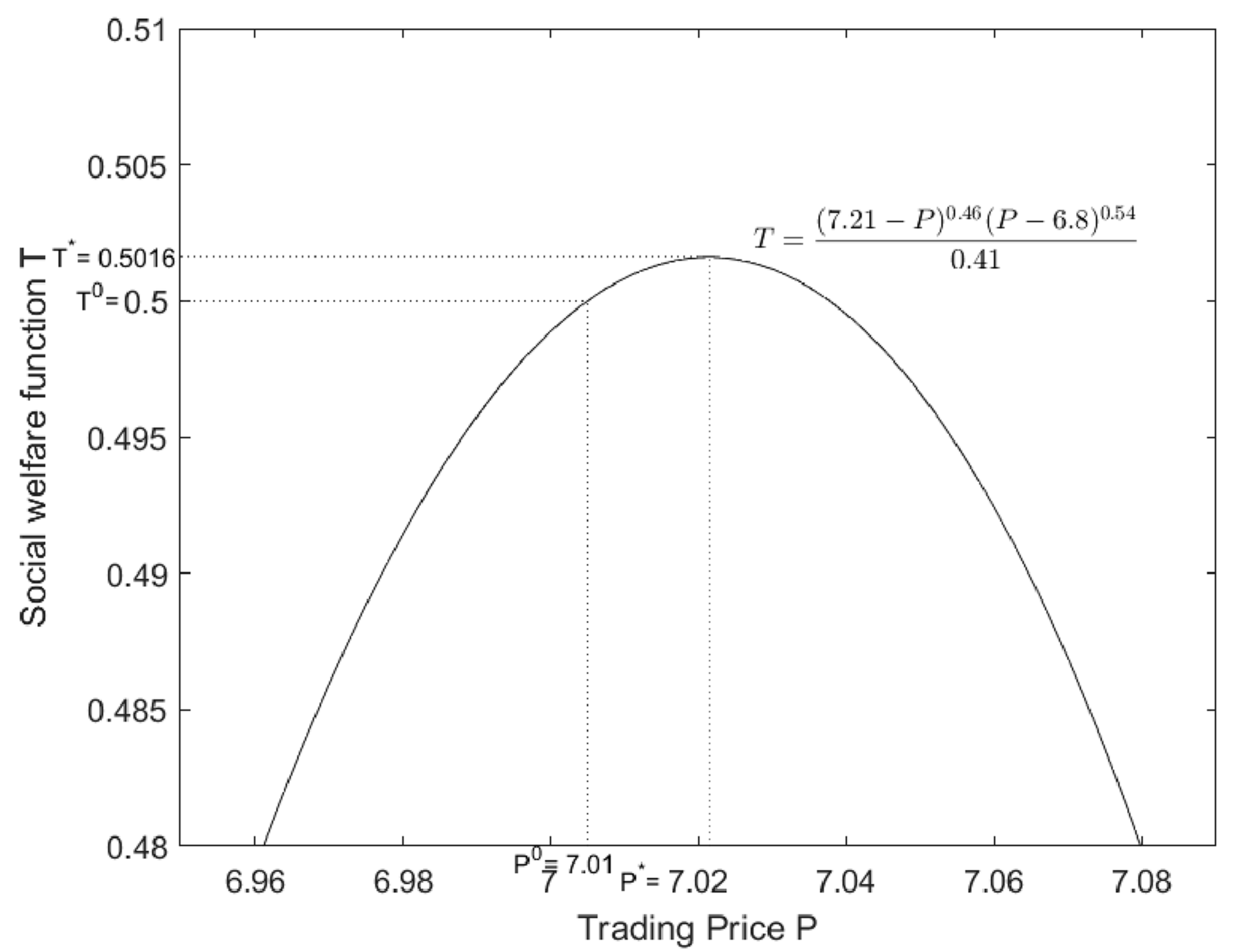

From the equilibrium price formula of the transaction mentioned in 3.1, the equilibrium prices of transactions 1 to 4 can be obtained as 6.26 RMB/m3, 7.47 RMB/m3, 6.84 RMB/m3, and 7.01 RMB/m3, respectively; meanwhile, the wealth utility function of Transaction 1 can be obtained according to Equations (6) and (7).

The wealth utility function for purchaser B1 is as follows.

The wealth utility function for seller S4 is as follows.

It can be obtained that the two parties to the transaction divide the expected profit (rather than the actual profit) according to a certain philosophy (in this paper, we choose the philosophy of the fairness of the flood distribution) to determine the optimal transaction price.

4.3.2. Social Welfare Function

We demonstrate the process of calculating the inequity pullback coefficient using the data of purchaser B1 and seller S4 in Transaction 1 (Table 3) as an example. According to Equation (9), the inequity pullback coefficient of purchaser B1 at the gross regional product level is calculated as follows.

The inequitable pullback coefficient of the selling side at the gross regional product level is the difference between 1 and this coefficient of the buying side B1, which can also be calculated by Equation (9), as follows.

The remaining dimensions of the first transaction and the unfair pullback coefficients involved in the second to fourth transactions were calculated using the same approach, as shown in Table 4.

From the above calculation process, it can be seen that the direct economic loss per GDP, land area, and population carried by purchaser B1 in the past three years is much larger than that of seller S4. The inequity pullback coefficient of purchaser B1 in these three aspects is much smaller than that of seller S4, as shown in Table 4. The inequity pullback coefficients of purchaser B1 and seller S4 are 0.03 and 0.97, indicating that the market focuses more on the seller’s utility in the process of trading drainage rights, i.e., the increase in social welfare per unit increase in utility on the seller’s side is much greater than that on the buyer’s side.

4.3.3. Optimal Transaction Price

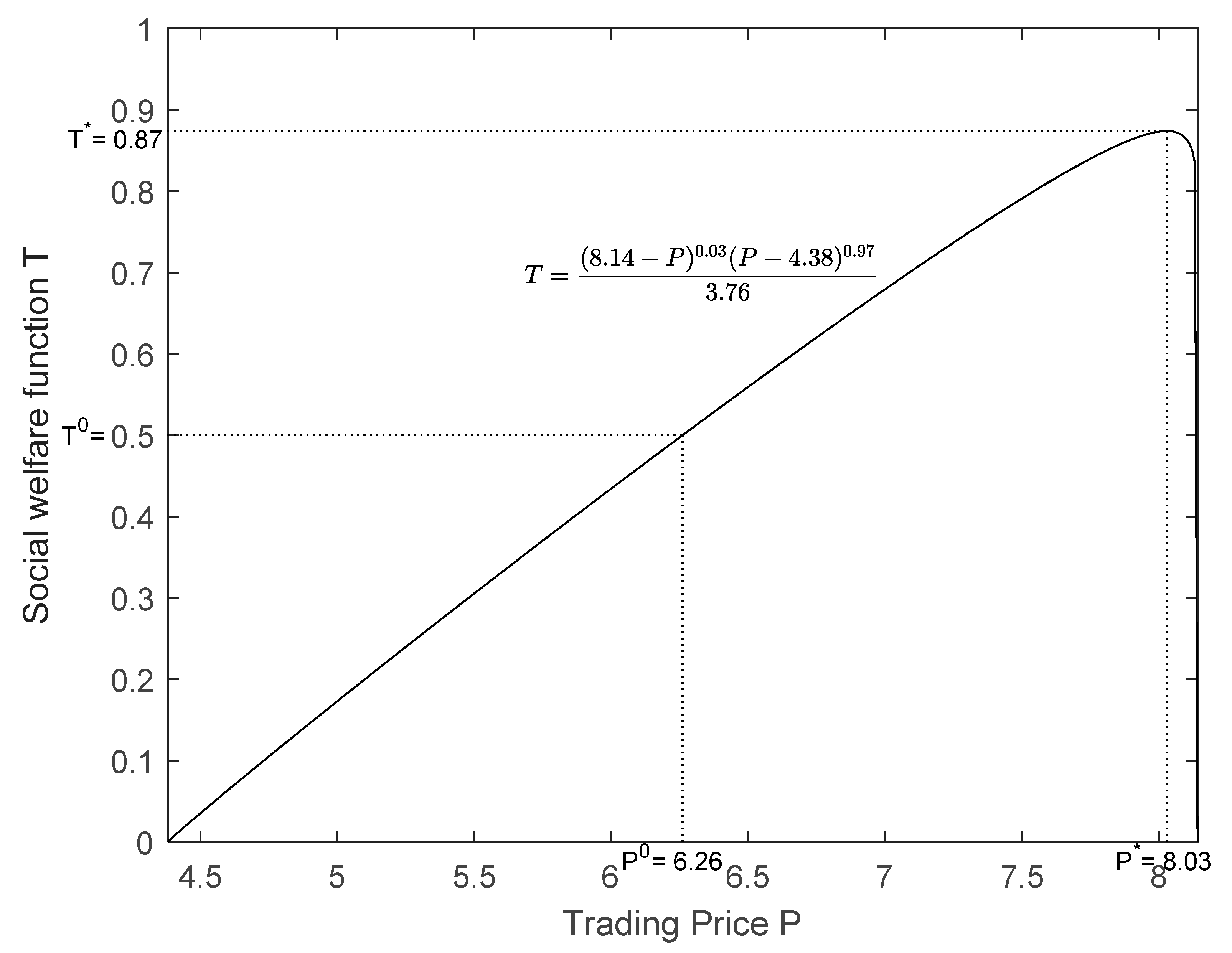

The optimal transaction price for the first transaction should be between 4.38 RMB/m3 and 8.14 RMB/m3 (as shown in Table 2). According to the previous section, the arithmetic means of the fair pullback coefficients of purchaser B1 and seller S4 are 0.03 and 0.97, respectively, indicating that the market pays more attention to the utility of the seller, i.e., expanding the expected profit margin of the seller, in the process of drainage rights trading. The optimal transaction price will occur well above the equilibrium trading price (6.26 RMB/m3).

As shown in Figure 1, the social welfare function for the first transaction shows an increasing and then decreasing trend, achieving a maximum social welfare value of 0.87 at 8.03. The optimal transaction price of 8.03 RMB/m3 is 0.07 RMB/m3 lower than the purchaser’s expected transaction price of 8.14 RMB/m3 and 3.65 RMB/m3 higher than the seller’s expected transaction price of 4.38 RMB/m3. From the perspective of the wealth utility function, it can be understood that the total wealth utility space of both sides of the transaction is 3.76 RMB/m3, among which the wealth utility space of the buyer is 0.07 RMB/m3, and the wealth utility space of the seller is 3.69 RMB/m3. When the optimal transaction price is 8.03 RMB/m3, the wealth utility acquisition degree of the buyer is 1.86% and the wealth utility acquisition degree of the seller is 98.14%, the wealth utility acquisition degree of the selling side is significantly higher than that of the buying side due to its larger fair pullback coefficient. From the perspective of the transaction itself, it can be understood that the buyer pays 0.07 RMB/m3 less for 1 m3 of drainage rights purchased, and the seller gets 3.65 RMB/m3 more for 1 m3 of drainage rights sold, and both sides of the transaction obtain certain wealth utility from the transaction and make the social utility at its maximum.

5. Conclusions

We found two shortcomings after combing through the existing studies. Firstly, the existing trading mechanism of drainage rights cannot solve the problem of simultaneous trading of multiple subjects, for which we have constructed a trading mechanism of drainage rights using a bilateral call auction model. Second, the existing pricing concept of drainage rights trading still takes the flood loss as the lower bound of the price. We broaden the idea and change the intrinsic concept of the model to focus on the degree of profit satisfaction for both buyers and sellers. Therefore, we constructed the pricing model using the wealth utility and social welfare function and drawing on the environmental Gini coefficient concept. The study’s results show that the trading mechanism model can give the optimal trading scheme when multiple subjects are trading drainage rights. This fills the gap in existing studies and can lead to efficient trading of drainage rights. At the same time, the pricing model can give the optimal transaction price that considers efficiency and fairness, providing a more practical pricing theory for drainage rights trading. In response to the above study, we give two policy recommendations. First, the government should establish good clearing rules so that the post-trade drainage pattern remains in the overall interest of the region. Second, the government should dig deeper into the factors that affect the fairness of drainage rights pricing and add more parameters to the pricing model. Of course, we found the following limitations of this study. When both parties are willing to trade and are satisfied with the transaction price, we consider the transaction to be established. In fact, if there is another subject between the geographic locations of the two parties to the transaction, we need to explore whether the parties need to pay a “toll” to this intermediary party. Therefore, we will explore this issue in-depth in our future research.

Author Contributions

Conceptualization, J.S. and T.Z.; methodology, T.Z.; software, F.S.; validation, J.S., T.Z. and T.Z.; formal analysis, T.Z.; investigation, J.S.; resources, F.S.; data curation, J.S.; writing—original draft preparation, F.S.; writing—review and editing, T.Z.; visualization, J.S.; supervision, J.S.; project administration, J.S.; funding acquisition, J.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Central Universities Basic Scientific Research Business Fund Special Project (No.2018B58814, No.2019B69214), the Social Science Foundation of Jiangsu Province (No.19GLD002), the Water Resources Science and Technology Project of Jiangsu Province (No.2019013), the National Social Science Foundation of China Major Project (No.17ZDA061), and the Decision-making Consulting Research Base Fund of Jiangsu Province (No.20SS1021).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

We thank the Institute of Environmental Accounting and Asset Management, Hohai University, for their solid data and funding support. The authors also thank the reviewers for their constructive suggestions to revise and improve the manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Luo, P.; He, B.; Takara, K.; Xiong, Y.E.; Nover, D.; Duan, W.; Fukushi, K. Historical assessment of Chinese and Japanese flood management policies and implications for managing future floods. Environ. Sci. Policy 2015, 48, 265–277. [Google Scholar]

- Scrase, J.I.; Sheate, W.R. Integration and integrated approaches to assessment: What do they mean for the environment? J. Environ. Policy Plan. 2010, 4, 275–294. [Google Scholar]

- Krieger, K. Putting Varieties of Risk-Based Governance into Institutional Context: The Case of Flood Management Regimes in Germany and England in the 1990s and 2000s. Ph.D. Thesis, King’s College London (University of London), Strand, London, UK, 2012. [Google Scholar]

- Zhang, M.; Wang, J. Global Flood Disaster Research Graph Analysis Based on Literature Mining. Appl. Sci. 2022, 12, 3066. (In Chinese) [Google Scholar]

- Yu, F.; Wang, Y.; Yuan, X.; Jiang, S. A preliminary investigation of the concept of drainage rights and its basic characteristics. J. Irrig. Drain. 2014, 33, 134–137. (In Chinese) [Google Scholar]

- Zhang, D.; Shen, J.; Sun, F.; Liu, B.; Wang, Z.; Zhang, K.; Li, L. Research on the Allocation of Flood Drainage Rights of the Sunan Canal Based on a Bi-level Multi-Objective Programming Model. Water 2019, 11, 1769. [Google Scholar]

- Zhang, D.; Shen, J.; Liu, P.; Sun, F. Allocation of Flood Drainage Rights Based on the PSR Model and Pythagoras Fuzzy TOPSIS Method. Int. J. Environ. Res. Public Health 2020, 17, 5821. [Google Scholar]

- Zhang, K.; Shen, J.; Han, H.; Zhang, J. Study of the Allocation of Regional Flood Drainage Rights in Watershed Based on Entropy Weight TOPSIS Model: A Case Study of the Jiangsu Section of the Huaihe River, China. Int. J. Environ. Res. Public Health 2020, 17, 5020. [Google Scholar]

- Zhang, D.; Shen, J.; Liu, P.; Zhang, Q.; Sun, F. Use of Fuzzy Analytic Hierarchy Process and Environmental Gini Coefficient for Allocation of Regional Flood Drainage Rights. Int. J. Environ. Res. Public Health 2020, 17, 2063. [Google Scholar]

- Sun, F.; Lai, X.; Shen, J.; Nie, L.; Gao, X. Initial allocation of flood drainage rights based on a PSR model and entropy-based matter-element theory in the Sunan Canal, China. PLoS ONE 2020, 15, e0233570. [Google Scholar]

- Zhang, J.; Zhang, C.; Liu, L.; Shen, J.; Zhang, D.; Sun, F. The necessity and feasibility of drainage rights allocation and trading in Jiangsu Province. Water Resour. Prot. 2019, 35, 5. (In Chinese) [Google Scholar]

- Lai, X.-P.; Sun, F.-H.; Shen, J.-Q.; Gao, X.; Zhang, D. Study on the influencing factors of regional drainage rights allocation based on WSR. Water Econ. 2020, 38, 8. (In Chinese) [Google Scholar]

- Jin, G.; Wang, P.; Zhao, T.; Bai, Y.; Zhao, C.; Chen, D. Reviews on land use change induced effects on regional hydrological ecosystem services for integrated water resources management. Phys. Chem. Earth 2015, 89–90, 33–39. [Google Scholar]

- Zhang, K.; Shen, J. Research on the management of drainage rights trading in China under quasi-markets—Based on the perspective of evolutionary game. J. Henan Univ. Soc. Sci. Ed. 2019, 4, 9. (In Chinese) [Google Scholar]

- Dong, C.; Huang, Y.-Y.; Zhao, Y.; Lu, H. Analysis of the development status of urban rainwater utilization at home and abroad. China Resour. Compr. Util. 2017, 35, 30–32. (In Chinese) [Google Scholar]

- Werritty, A. Sustainable flood management: Oxymoron or new paradigm? Area 2006, 38, 16–23. [Google Scholar]

- Porter, J.; Demeritt, D. Flood-risk management, mapping, and planning: Theinstitutional politics of decision support in England. Environ. Plan. A 2012, 44, 2359–2378. [Google Scholar]

- Buuren, A.V.; Ellen, G.J.; Warner, J.F. Path-dependency and policy learning in the Dutch delta: Toward more resilient flood risk management in the Netherlands? Ecol. Soc. 2016, 21, 43. [Google Scholar]

- Shen, J.; Zhan, Q.; Cao, Q.; Sun, F.; Zhang, K.; Zhang, D.; Zhao, M. The pricing method of drainage rights trading based on full cost method and its application. Water Econ. 2022, 40, 7. (In Chinese) [Google Scholar]

- Shen, J.; Wang, X.; Sun, F. Research on the pricing method of drainage rights trading in China under quasi-market. Water Econ. 2021, 39, 7. (In Chinese) [Google Scholar]

- Scrase, J.I.; Sheate, W.R. Re-framing Flood Control in England and Wales. Environ. Values 2005, 14, 113–137. [Google Scholar]

- Zhang, Y.; Guo, R. Scientific drainage to improve urban flooding in the UK. Henan Water Resour. South-North Water Divers. 2011, 19, 48. (In Chinese) [Google Scholar]

- Wlliott, A.H.; Trowsdale, S.A. Areview of models for low impact urban stormwater grainage. Environ. Model. Softerware 2007, 22, 394–405. [Google Scholar]

- Wang, H.-F.; Fan, Z.-W.; Luo, L.; Zhang, W. The inspiration of foreign urban rainwater utilization financial support policy to China. Water Resour. Dev. Res. 2014, 14, 12–15. (In Chinese) [Google Scholar] [CrossRef]

- Sun, F.; Du, X.; Shen, J. An asymmetric information bargaining model for pricing drainage rights transactions based on fair preferences. Resour. Ind. 2020, 22, 10. (In Chinese) [Google Scholar]

- Tian, G.; Liu, J.; Wei, B. Pricing and simulation of water discharge rights in Taihu Lake basin based on improved bilateral bidding auction model. Ecol. Econ. 2020, 36, 6. (In Chinese) [Google Scholar]

- Chen, W.; Cao, S. Application of improved bilateral call auction model in water rights trading. China Rural. Water Conserv. Hydropower 2010, 3, 3. (In Chinese) [Google Scholar]

- Son, Y.S.; Baldick, R.; Siddiqi, S. Reanalysis of “Nash Equilibrium Bidding Strategies in a Bilateral Electricity Market”. Ieee Trans. Power Syst. 2004, 19, 1243–1244. [Google Scholar]

- Markus, V. Utility of wealth with many indivisibilities—ScienceDirect. J. Math. Econ. 2017, 71, 20–27. [Google Scholar]

- Estimation of Direct and Indirect Economic Losses Caused By a Flood With Long-lasting Inundation: Application To the 2011 Thailand Flood. Ecol. Environ. Conserv. 2020, 56, e2019WR026092.

- Smith, A. On the Division of Labour. In The Wealth of Nations, Books I–III; Penguin Classics: New York, NY, USA, 1986; p. 119. [Google Scholar]

- Hirai, H.; Sato, R. Polyhedral Clinching Auctions for Two-Sided Markets. Math. Oper. Res. 2021, 47, 259–285. [Google Scholar]

- Wu, F.; You, M.; Yu, Q. A study on wealth utility-based pricing model of emission rights under multiple scenarios. Soft Sci. 2017, 31, 108–111, 140. (In Chinese) [Google Scholar] [CrossRef]

- Grant, A.; Satchell, S. Investment decisions when utility depends on wealth and other attributes. Quant. Financ. 2020, 20, 499–513. [Google Scholar]

- Pollak, R.A. Bergson-Samuelson Social Welfare Functions and the Theory of Social Choice. Q. J. Econ. 1979, 93, 73–90. [Google Scholar]

- Nash, J.F. The Bargaining Problem. Econometrica 1950, 18, 155–162. [Google Scholar]

- Gini Coefficient Analysis of Regional Differences in Energy Utilization Under the Concept of Low-carbon Ecological Environmental protection. Ecol. Environ. Conserv. 2019, 28, 2149–2160.

- Wu, F.; Cao, Q.D.; Zhang, D.; Sun, F.; Shen, J. Allocation of drainage rights of the Sunan Canal based on environmental Gini coefficient. J. Henhai Univ. Nat. Sci. Ed. 2020, 48, 6. (In Chinese) [Google Scholar]

Figure 1.

Schematic diagram of the optimal transaction price.

Figure 2.

Schematic diagram of the optimal transaction price.

Figure 3.

Schematic diagram of the optimal transaction price.

Figure 4.

Schematic diagram of the optimal transaction price.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Set of quotes ranked by expected transaction price.

| Buyer Bi | Seller Sj | ||||

|---|---|---|---|---|---|

| Buyer | Expected Acquisition Price oi (yuan/m3) | Expected Acquisition Volume xi (m3) | Seller | Expected Sales Price fj (yuan/m3) | Expected Sales Volume yj (m3) |

| B1 | 8.14 | 100 | S4 | 4.38 | 37.5 |

| B3 | 7.21 | 100 | S3 | 6.47 | 50 |

| B2 | 5.83 | 50 | S2 | 6.80 | 75 |

| B4 | 5.20 | 62.5 | S1 | 9.45 | 100 |

Table 2.

List of transactions.

| Transaction Serial Number | Buyer Bi | Seller Sj | Expected Trading Volume (m3) | Expected Acquisition Price oi (yuan/m3) | Expected Sales Price fj (yuan/m3) |

|---|---|---|---|---|---|

| I | B1 | S4 | 37.5 | 8.14 | 4.38 |

| II | B1 | S2 | 62.5 | 8.14 | 6.80 |

| III | B3 | S3 | 50 | 7.21 | 6.47 |

| IV | B3 | S2 | 12.5 | 7.21 | 6.80 |

Table 3.

Data on the unfair pullback coefficient of GDP for B1 and S4.

| Indicators (Arithmetic Average of the Previous Three Years) | B1 | S4 |

|---|---|---|

| GDP (100 million yuan) | 5911.45 | 2392.48 |

| Land area (km2) | 3063 | 3012 |

| Population (10,000 people) | 336.2 | 222.01 |

| Flooding direct economic loss (100 million yuan) | 1.44 | 0.03 |

Table 4.

Calculation results of unfair pullback coefficient.

| Indicators | Transaction I | Transaction II | Transaction III | Transaction IV | ||||

|---|---|---|---|---|---|---|---|---|

| B1 | S4 | B1 | S2 | B3 | S3 | B3 | S2 | |

| GDP | 0.05 | 0.95 | 0.36 | 0.64 | 0.58 | 0.42 | 0.1 | 0.9 |

| Land | 0.02 | 0.98 | 0.37 | 0.63 | 0.80 | 0.20 | 0.73 | 0.27 |

| Population | 0.03 | 0.97 | 0.39 | 0.61 | 0.65 | 0.35 | 0.56 | 0.44 |

| Average | 0.03 | 0.97 | 0.37 | 0.63 | 0.67 | 0.33 | 0.46 | 0.54 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Shen, J.; Zhu, T.; Sun, F. A Study on the Mechanism and Pricing of Drainage Rights Trading Based on the Bilateral Call Auction Model and Wealth Utility Function. Water 2022, 14, 2269. https://doi.org/10.3390/w14142269

AMA Style

Shen J, Zhu T, Sun F. A Study on the Mechanism and Pricing of Drainage Rights Trading Based on the Bilateral Call Auction Model and Wealth Utility Function. Water. 2022; 14(14):2269. https://doi.org/10.3390/w14142269

Chicago/Turabian StyleShen, Juqin, Tingting Zhu, and Fuhua Sun. 2022. "A Study on the Mechanism and Pricing of Drainage Rights Trading Based on the Bilateral Call Auction Model and Wealth Utility Function" Water 14, no. 14: 2269. https://doi.org/10.3390/w14142269

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.