Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

If you’re one of the 57 million people who freelance or are self-employed, you might run into challenges when applying for a mortgage. That’s because without a W-2, it’s harder to prove you have a steady income.

Although self-employed mortgage applicants must take extra steps during the mortgage process, it’s still possible to secure financing for your next home.

Here are 8 steps to getting a mortgage as an independent contractor:

- Know what lenders want from self-employed applicants

- Improve your credit score

- Lower your debt-to-income ratio

- Try to save up for a higher down payment

- Gather all your documentation

- Consider a low-doc or no-doc mortgage

- Consider applying with a co-borrower

- Shop around for the best rates

1. Know what lenders want from self-employed applicants

Lenders ultimately want to make sure self-employed mortgage borrowers have stable income that they can rely on for the foreseeable future.

When applying for a home loan, borrowers will generally need to show at least two years’ worth of uninterrupted self-employment income. That helps lenders see that the borrower is in overall good financial health.

2. Improve your credit score

Credit scores play a big role in whether an applicant qualifies for a mortgage and the interest rate they get. Lenders might not have a target credit score specifically for self-employed people, but they’re generally looking for a score of at least 620.

Because lenders are tightening standards, you might need a higher credit score these days. The average FICO credit score among mortgage borrowers in September 2020 was 767, according to Ellie Mae.

Here are some ways you can improve your credit: Learn More: Credit Score Needed to Get a Home Loan Your debt-to-income ratio measures how much of your monthly income goes toward debt payments. This number helps lenders determine if you can comfortably afford a mortgage payment. There are two types of DTI ratios: Let’s say you earn $5,000 a month before taxes. You pay $300 a month toward student loans and $350 for an auto loan, and your estimated future monthly mortgage payment is $1,200. Here’s how you calculate both ratios: Front end: $1,200 / $5,000 = 0.24 x 100 = 24% Back end: ($300 + $350 + $1,200) / $5,000 = 0.37 x 100 = 37% If you need to improve your DTI ratio to qualify for a mortgage, work on paying down your debts and increasing your income. While you can put down as little as 3% with some types of mortgages, a higher down payment offers several benefits: If you’re having trouble coming up with a down payment, check out down payment assistance programs. These are geared toward first-time homebuyers, but repeat homeowners might also qualify. Lenders will require extensive documentation from self employed mortgage loan borrowers to verify their income and make sure the borrower can make their mortgage payments. Before heading to a lender, do a little prep work by gathering these documents: The lender will look for taxable income and may subtract anything that doesn’t seem stable and consistent. The lender might also request a W-2 from your previous employer. With a strong work history in the same field — proven with the W-2 form — you might be able to get a home loan with as little as 12 months of self-employed work. A “low-documentation loan” or “no-documentation loan” allows self-employed borrowers to apply for a mortgage without extensive financial documentation. In lieu of tax returns, lenders may review your assets, ask you to state your income, or base the loan entirely on the collateral. There are four types of low- and no-doc mortgages: It might be difficult to find a lender that offers such mortgages, and they may come with higher credit score requirements than traditional mortgages. Additionally, the interest rate might be up to 3 percentage points higher than a loan with a standard rate. A self-employed borrower who applies for a mortgage with a co-borrower — a spouse, for example — might be able to sidestep some of these documentation requirements. Your co-borrower should have a W-2 that shows they earn enough to comfortably cover the mortgage payments along with other household expenses. Having little to no debt and a good amount of cash reserves will also boost your chances of approval. Check mortgage rates: When it comes to finding the best interest rate on home loans, shopping around can help you save hundreds or even thousands of dollars.

3. Lower your debt-to-income ratio

4. Try to save up for a higher down payment

Credible makes finding a mortgage easy

Compare prequalified mortgage rates from top lenders in just 3 minutes.

5. Gather all your documentation

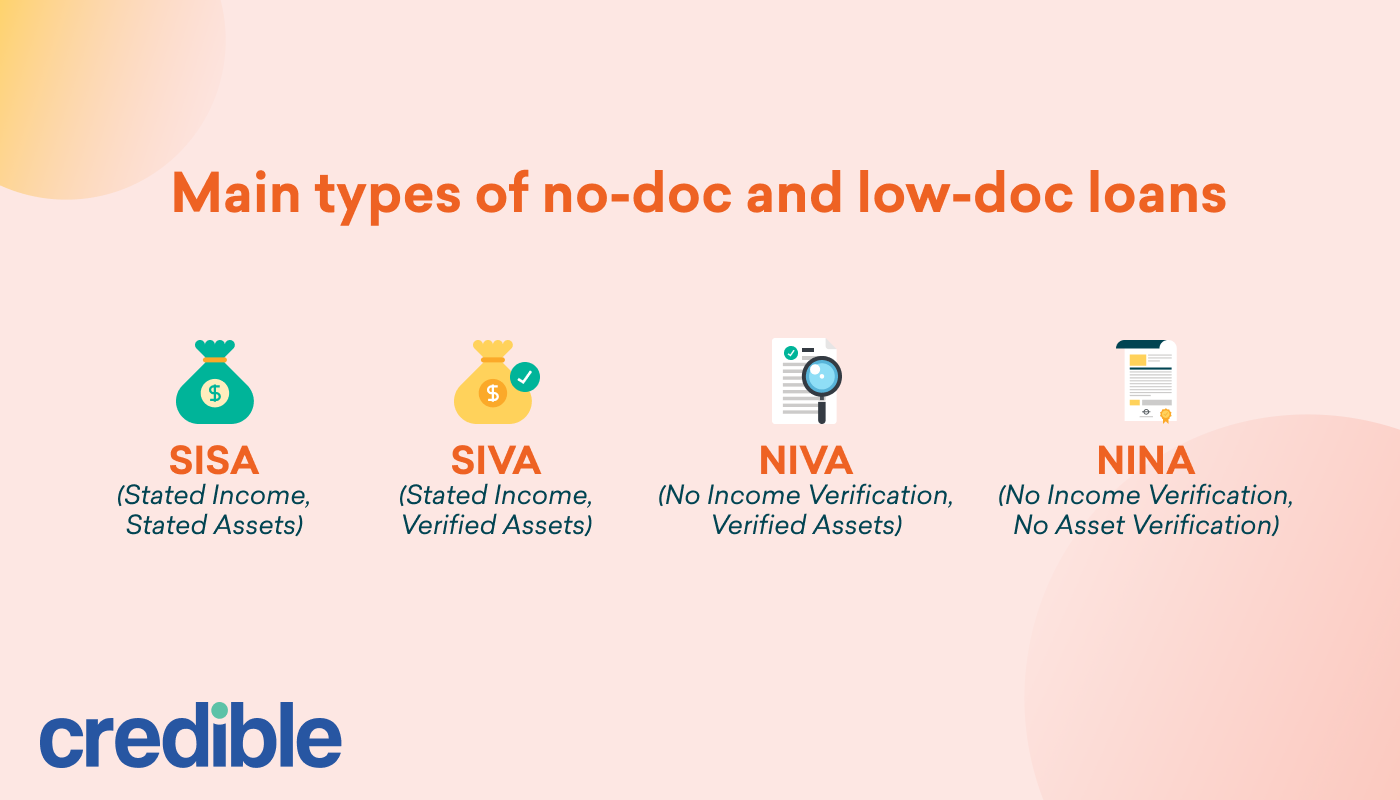

6. Consider a low-doc or no-doc mortgage

7. Consider applying with a co-borrower

8. Shop around for the best rates

![]()