The paper summarized here is part of the Fall 2022 edition of the Brookings Papers on Economic Activity (BPEA), the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. The conference draft of this paper was presented at the Fall 2022 BPEA conference. The final version was published in the Fall 2022 issue by Johns Hopkins University Press.

See the Fall 2022 BPEA event page to watch conference recordings and read conference drafts of all the papers from this edition. Submit a proposal to present at a future BPEA conference here.

Read final paper with comments, discussion summary and online appendix here»

Download data/programs for main paper here»

Download data/programs for Furman comment here»

Download data/programs for Şahin comment here»

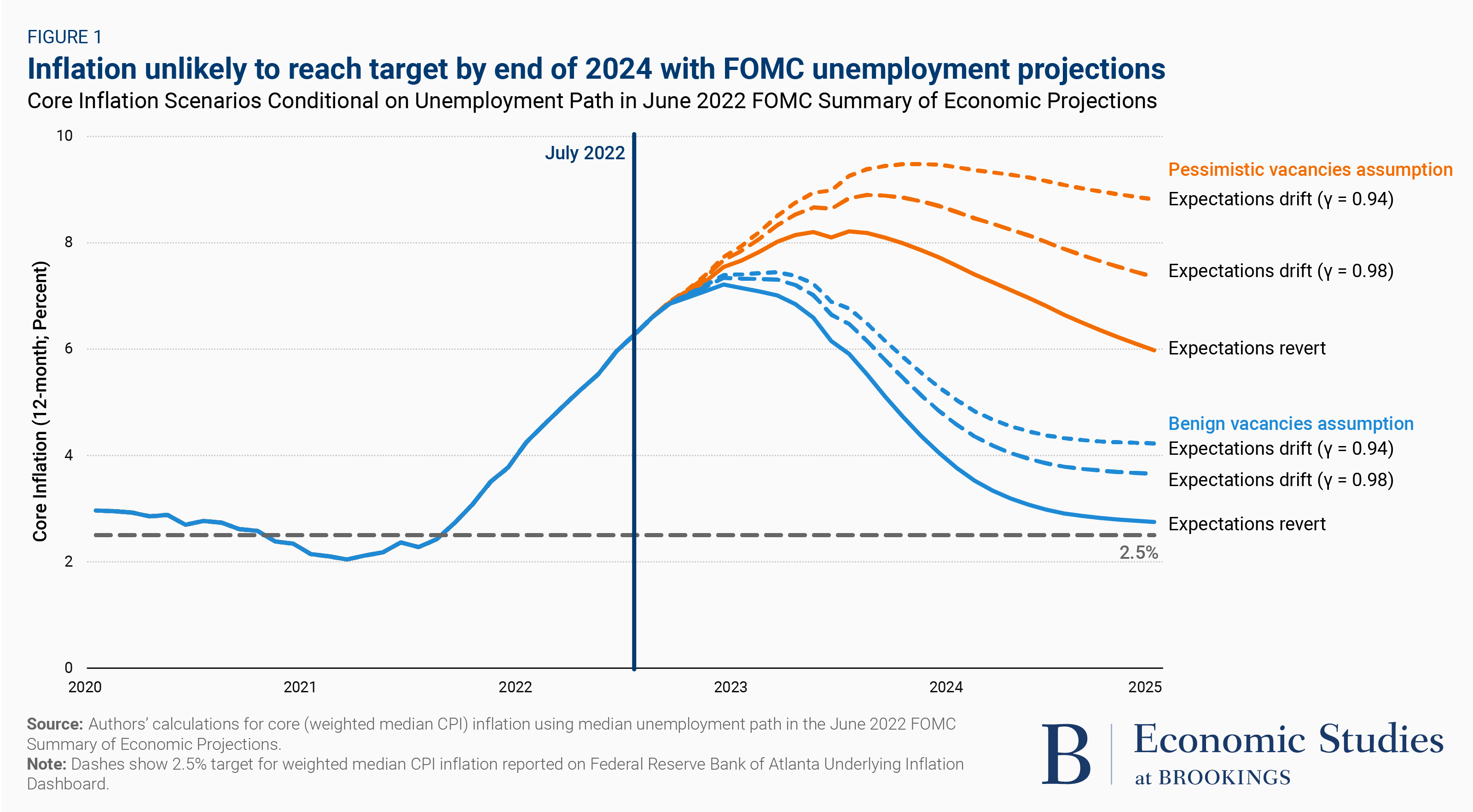

The Federal Reserve likely will need to push unemployment far higher than its 4.1 percent projection if it is to succeed in bringing inflation down to its 2 percent target by the end of 2024, suggests a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 8.

The paper, Understanding US Inflation During the COVID-19 Era, analyzes why the pandemic-related surge in inflation has persisted and runs simulations under different assumptions to look at where inflation might be heading.

According to the authors—Laurence Ball of Johns Hopkins University and Daniel Leigh and Prachi Mishra of the International Monetary Fund—it is unlikely, but not impossible, for the Fed to achieve the soft landing (substantially lower inflation with only modestly higher unemployment) that it projected in June.

The median Fed policymaker projected 4.1 percent unemployment at the end of 2024, up only modestly from 3.7 percent in July. The median projection for inflation, as measured by the Commerce Department’s personal consumption expenditures (PCE) price index, was 2.2 percent at the end of 2024, down from a four-decade high of 6.8 percent in June. The PCE Index eased modestly in July (prices were up 6.3 percent from a year earlier). The Labor Department’s more widely known consumer price index (CPI) also hit a 40-year high in June (9.1 percent) before easing slightly to 8.5 percent in July.

“If either the labor market doesn’t behave, or expectations don’t behave, the small increase in unemployment the Fed projects won’t be enough.”

So far this year the Fed has raised its short-term interest rate target by 2.25 percentage points, from near zero, and projected in June that to tame inflation it would need to raise the target by only an additional percentage point this year and a half percentage point next year.

Fed policymakers, as well as most economists (including the paper’s authors), had expected that the upturn in inflation that began in March 2021 would prove transitory. The paper cited three reasons why those expectations proved to be wrong: first, unforeseeable events such as Russia’s invasion of Ukraine and the persistence of pandemic supply-chain disruptions; second, failure to account for the pass-through of specific price shocks (such as to energy and auto prices) into the core, or underlying, rate of inflation; and, third a focus on the unemployment rate (which has only recently fallen back to pre-pandemic levels) as an indicator of labor market tightness rather than the very high ratio of job vacancies to unemployed workers (V/U).

The very high V/U ratio in 2021 and this year can explain three-quarters of the rise in monthly core CPI inflation as measured by a Federal Reserve Bank of Cleveland index that strips out the effects of unusually large price changes in certain industries, according to the paper. Some of the consumer demand that fueled the economy, as well as the labor market tightness, in turn, can be explained by the Biden administration’s $1.9 trillion American Rescue Plan enacted in March 2021. Without it, the authors estimate that annualized monthly core inflation would have been 3.7 percent in July rather than 6.5 percent.

According to the paper, whether the Fed can achieve its objectives depends on whether it is possible to slow demand in such a way that vacancies decrease but unemployment doesn’t rise (returning the V/U ratio to its pre-pandemic norm) and on whether consumers and businesses start to expect that high inflation will continue for the longer term, and thus plan for it. Under optimistic assumptions for both the V/U ratio and long-term inflation expectations (and assuming the Fed’s 4.1 percent unemployment projection proves correct), the paper projects the Fed will bring core inflation down close to its target by the end of 2024. However, under the most pessimistic assumptions for both the V/U ratio and inflation expectations, core inflation rises to about 8.8 percent if unemployment moves up only to 4.1 percent.

“If you make quite-optimistic assumptions, we might get something close to what the Fed expects,” Ball said in an interview with The Brookings Institution. “But if either the labor market doesn’t behave, or expectations don’t behave, the small increase in unemployment the Fed projects won’t be enough. Either inflation will stay substantially higher, or we will have higher unemployment and a substantial economic slowdown.”

Citations

Ball, Laurence, Daniel Leigh, and Prachi Mishra. 2022. “Understanding US Inflation during the COVID-19 Era.” Brookings Papers on Economic Activity, Fall. 1-54.

Furman, Jason. 2022. “Comment on ‘Understanding US Inflation during the COVID-19 Era’.” Brookings Papers on Economic Activity, Fall. 55-65.

Şahin, Ayşegül. 2022. “Comment on ‘Understanding US Inflation during the COVID-19 Era’.” Brookings Papers on Economic Activity, Fall. 65-76.

Authors

Discussants

-

Acknowledgements and disclosures

Daniel Leigh and Prachi Mishra are employees of the International Monetary Fund, which conducts a review of all externally published pieces. The authors did not receive financial support from any firm or person for this article or from any firm or person with a financial or political interest in this article. The authors are not currently an officer, director, or board member of any organization with a financial or political interest in this article.

David Skidmore authored the summary language for this paper. Becca Portman assisted with data visualization.