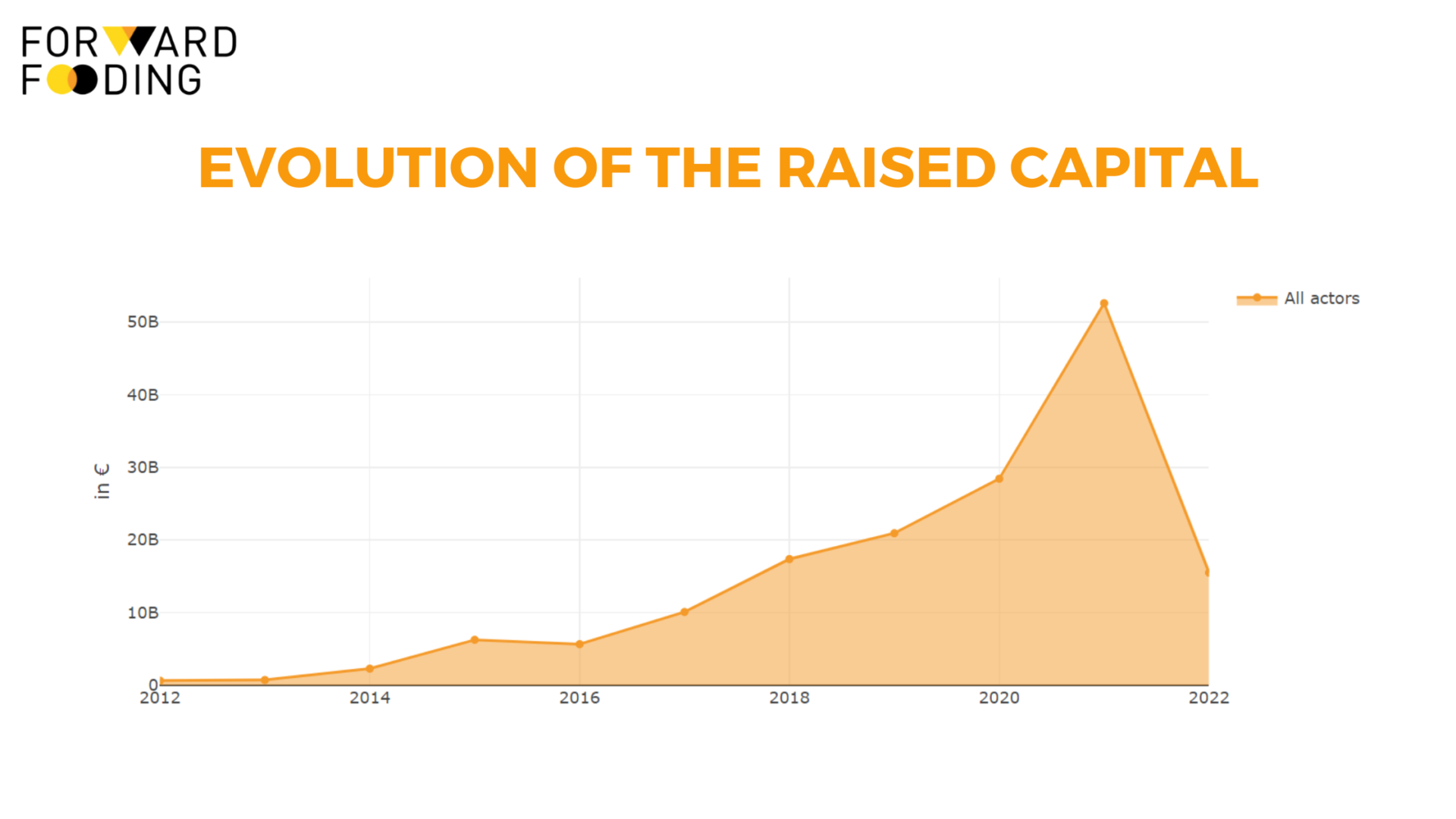

When we first started Forward Fooding back in 2015, ‘FoodTech’ or ‘AgriFoodTech’ didn’t really mean much to most people and were mostly used as buzzwords to describe any sort of product or service that was somehow combining food and technology. While startups in this field started burgeoning in the early 2010s, investments in the space only really started to take off in 2016, as evidenced in our FoodTech Data Navigator. Indeed 93% of the $163B invested in the sector to date were deployed over the past 5 years, and this is also when 70% of all AgriFoodTech companies were founded. Over this 2016-2021 period, AgriFoodTech funding has been growing at an impressive 56% CAGR.

And yet the FoodTech sector received only one third as much funding when compared to the FinTech industry during the same timeframe. One could argue that this large funding differential points to a less mature startup ecosystem and industry but the reality is slightly different simply because the FoodTech ecosystem followed a different evolutionary path.

Source: Forward Fooding FoodTech Data Navigator

We don’t like to brag about our knowledge of the sector but we have been actively fostering the global FoodTech ecosystem and observing its development since 2013 when our CEO moved to the Bay Area for work and ended up founding the world’s first investment platform for food and FoodTech startups (you can read more on his medium here). Thus, over the last decade, we have been lucky enough to witness how we went from using FoodTech as a buzzword to creating and fostering the largest community of FoodTech innovators in the world by working elbow-by-elbow with the operators who have made this sector, and went from mapping a handful of impact-driven angel investors to a record-breaking number of dedicated VC funds.

The first wave of FoodTech investment

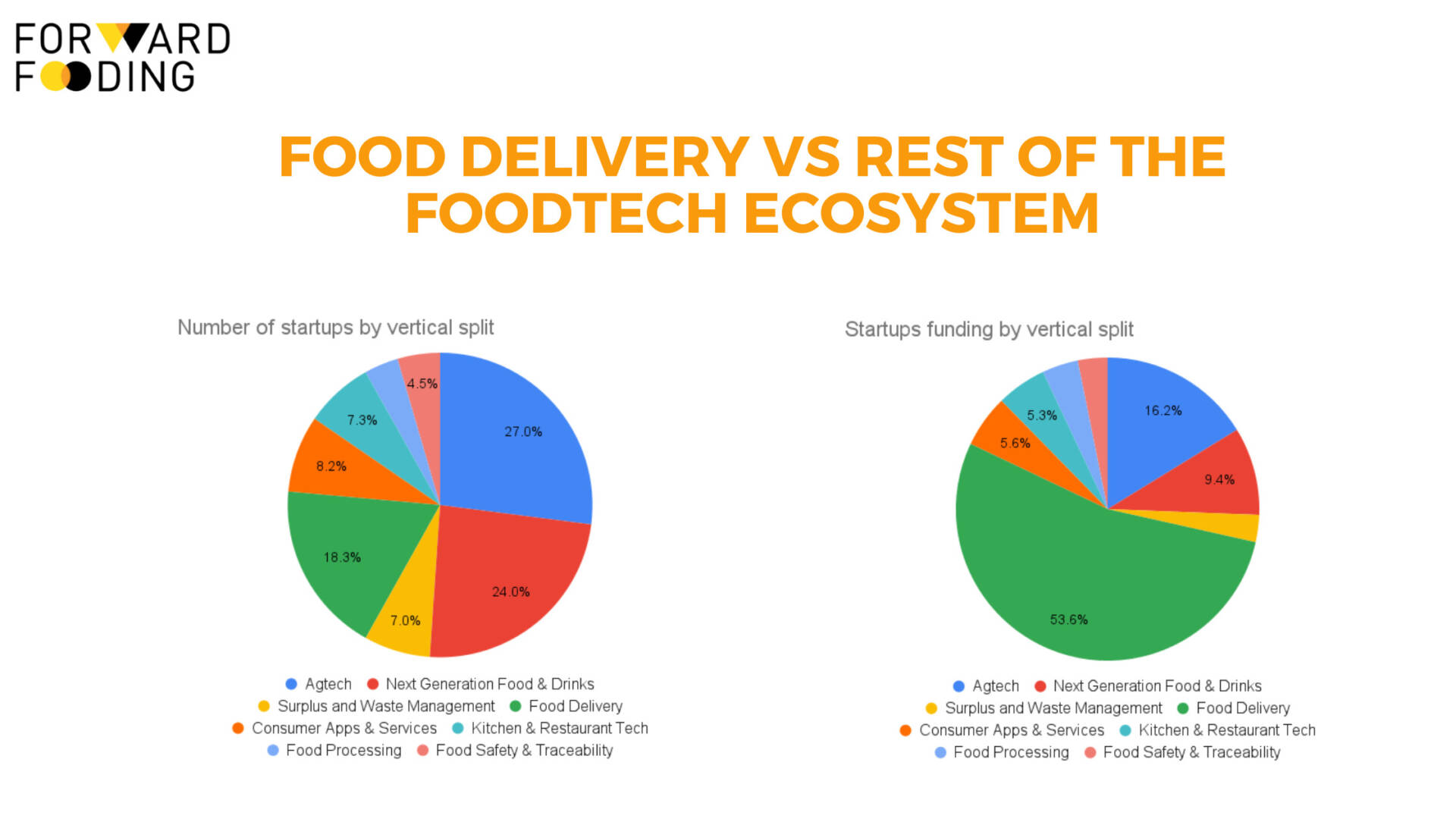

Looking at where the capital has been injected more specifically, I like to think in terms of ‘waves’. Without any doubt, the ‘First wave’ of FoodTech investment was dominated by the Food Delivery sector, which, since 2012, attracted more than 54% of total FoodTech funding. While it represents less than 20% of the total number of companies in the FoodTech space, Food Delivery contributed to raising awareness and turning FoodTech into a ‘sector’ in itself in investors’ minds most likely because of the popularity that the delivery services have gained among consumers.

Source: Forward Fooding FoodTech Data Navigator – 2012 to 2022

The e-grocery subsector alone received $11.5B in 2021. Yet, we have probably reached the crest of this wave. As explained in a recent blogpost, investors are raising concerns about the unit economics and valuations of companies in this sector – resonating with the work of Pr. Tom Eisenmann , who reminds us that these business models have been tried already, and they failed when they couldn’t achieve positive unit economics. Instant delivery companies are particularly on the radar, prime suspects here, as the likes of Getir, Gorillas, or Jokr are accumulating large losses. And recently letting go hundreds of employees as they forcibly downsize their operations.

Gorillas delivery worker

Gorillas delivery worker

As a consequence, we should expect an even stronger wave of consolidation in the Food delivery sector, which has already started a few years ago (e.g multiple acquisitions of Doordash and DeliveryHero). This phenomenon is happening both vertically (tech acquisition like robotics or operations management platforms to achieve more efficiency and reduce costs) and horizontally (to acquire market shares and expand in other sub-sectors). I personally think it is realistic to imagine that in 5 years time, we could have less than 10 major players offering different delivery services as a one-stop-shop solution (from food delivery from restaurants and dark kitchens to groceries), covering the entire global market.

Ultimately, we expect investors to redirect their capital towards other segments of FoodTech. And at this level, the shift towards the ‘second wave,’ the alternative protein sector, is already well underway.

The second wave (alternative proteins) and its ‘hybrid revolution’ is well underway

Source: Forward Fooding FoodTech Data Navigator

As shown in the graph above, 87% of all the capital invested in alternative proteins was invested between 2019 and today (2022). This capital inflow went to 3 main pillars of the alternative protein sector: plant-based, protein fermentation, and cellular agriculture (if you aren’t too familiar with what alternative proteins are all about, this blogpost is a good refresher). This movement started in the US in 2011 and was led by major players such as plant-based meat leaders Impossible Foods and BeyondMeat, protein fermentation company Perfect Day, or cell-based meat maker Upside Foods.

Some of the alternative protein top-funded companies

Yet, if you are following the sector closely, you will also witness that the investment landscape has started to evolve within the alternative proteins sector itself. First of all, as Big Food companies and retailers are entering the space, we can expect the plant-based sector to mature and become saturated. This will leave space only for the most funded players such as Impossible, Beyond or NotCo, and for ‘local’ champions such as Heura in Spain, La Vie in France or THIS in the UK.

In addition, according to recent data from the Plant-based Foods Association, global growth in annual retail dollar sales has been slowing down from 33% in 2020 to 17% in 2021 (equivalent to $5.6 billion). As highlighted by Tyler Morgan, partner at Boulder Food Group, some doubts are also starting to emerge when it comes to the actual size of the market and to consumers’ long term adoption:

“There are good intentions behind these businesses, but the market is smaller than people imagined. The market can’t support 100 alternative meat businesses. It can barely support that many animal meat businesses and that industry is 30 times the size.”

The ‘Hybridization’ of alternative protein products – the solution to consumer adoption and scalability?

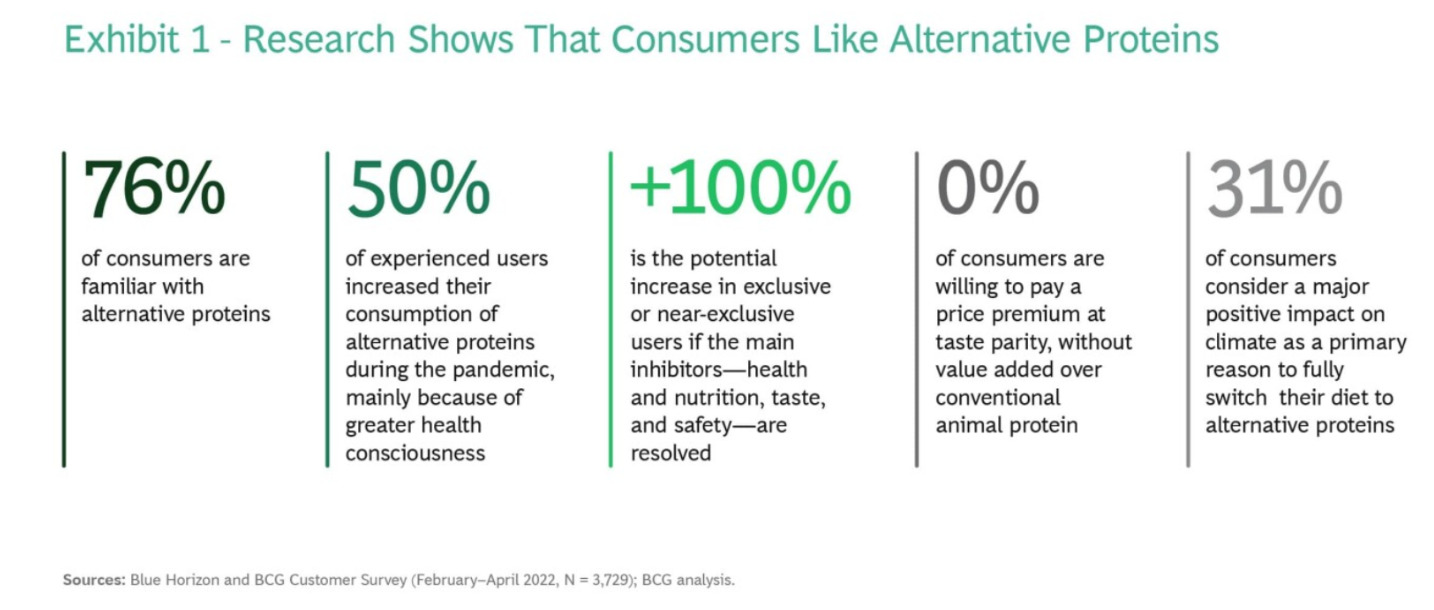

As the meat and dairy alternative segments are becoming more and more difficult to enter and consumers more demanding, the key differentiators aside from price parity with animal-based products, reside more than ever in taste, texture, nutritional value, clean label & environmental impact. This point was also highlighted in a recent customer survey from BCG.

The last statistic in the table above is particularly important: a lower carbon footprint could become a key, if not the key, selling point for alternative proteins, as consumers have become increasingly climate conscious in their choices. While alternative proteins companies will continue trying to rival animal proteins in taste, texture, nutritional value and price parity, if there is one area in which alternative proteins “beat” animal proteins hands down it is their carbon footprint. And indeed the same BCG study evidences that among all sectors and industries out there, from cement to aviation, alternative proteins offer by far the largest potential to reduce our global carbon emissions:

As a consequence, alternative protein products are now becoming ‘hybrids,’ leveraging different technologies, such as precision fermentation, 3D printing and new ingredients to make products that are intrinsically much more planet-friendly. while being closer, or yet better, to their meat and dairy counterparts in terms of taste, mouthfeel and nutritional value. This ‘hybridiation’ process comes also with the additional advantage of making these companies’ technologies more scalable.

For example, Impossible Foods’s ‘secret ingredient,’ their plant-based heme, is made via fermentation of genetically engineered yeast, giving the Impossible burger its ‘bloody’ feel. On the other hand, companies like Redefine Meat or Revo Foods leverage 3D printing, as opposed to the widely-used ‘extrusion’ (processing technique using moisture, high heat and mechanical energy to produce meat substitutes in a matter of seconds), in order to achieve a more realistic texture. Other companies focused on the nutritional values including Heura, which uses olive oil (instead of coconut or palm oil) as a healthier fat analog , or Dutch Weed Burger, which enriches their product with seaweed extract for both nutritional and taste purposes.

Revo Foods Plant-based salmon

Revo Foods Plant-based salmon

There are two natural consequences here, which we already see thanks to our proprietary data from the FoodTech Data Navigator : first, we are witnessing more and more B2B companies emerging in the sector, and second, more and more capital directed towards them.

Indeed, many of the ‘enablers’ of these ‘hybrid’ products, are pure B2B players such as ingredient providers or tech enablers that focus on specific angles rather than trying to replicate the entire products. And they can be grouped mostly into 1. fermentation and 2. cellular agriculture technologies.

Source: Forward Fooding FoodTech Data Navigator

These include, for example, fungi fermentation companies such as Mycotechnology or Mycorena – the latter being the first one to specifically recreate a fat analog from fungi, on top of enriched protein ingredients for plant-based meat analogues (we think fungi fermentation is a very fascinating technology – here is an article that tells you why).

Mycorena’s fungi based protein

Mycorena’s fungi based protein

Other examples could come from companies leveraging cellular agriculture to reproduce animal fat such as Cubiq Foods or Hoxton Farms. Or companies like Biftek, which focuses on creating animal-free ‘growth medium’ (the component that allows cells to reproduce), aiming to replace the extremely expensive ‘Fetal-Bovine-serum’, which remains currently one of the main obstacles to cell-based meat scalability. Or yet, companies leveraging different fermentation technics to make protein concentrate out of thin air (yes, ‘air protein’ is a thing) such as Solar Foods, amongst many others.

Solar Foods’ ‘air-based’ protein

Solar Foods’ ‘air-based’ protein

Looking at investment data, a growing focus on fermentation and cellular agriculture is clearly being reflected, as 70% to 80% of the total capital injected over time for these 2 sub-clusters was invested over in the past 18 months (2020-2022).

Source: Forward Fooding FoodTech Data Navigator

Yet, looking at the amount of capital invested in terms of volume, the plant-based proteins sub-sector is still far ahead of fermentation and cellular agriculture, as highlighted in a recent report from Agfunder:

‘”Plant-based proteins — including pea, oat, and soy-based products — grabbed almost half of all European alt-protein funding in 2021, raising just over $200 million. The sub-category’s lead isn’t surprising, as plant-based ingredients remain the fastest, most tested way for alt-protein to get to market.’’

Another key ‘shift’ to note is the growing importance of partnerships within the alternative proteins sector. We are indeed witnessing more and more active collaborations between companies. Amongst the most recent examples, cell-based meat company MeaTech and fungi fermentation company Enough signed a joint development agreement to accelerate MeaTech’s ambitions of launching hybrid meat products made with cell-based fat, while another recent interesting collaboration is between Siimpligood, company producing fresh spirulina biomass, and the international food conglomerate IFF-DuPont, for the co-development of a smoked salmon analog made entirely from whole fresh spirulina.

MeaTech’ 3D printing technology

The growing number of partnerships and an investment shift towards ingredients and tech enablers is net positive for the sector, as it will ultimately help driving greater scalability, better products, more adoption from consumers, and hence generate a much bigger impact.

While reading this article you might wonder: is FoodTech just about food delivery and alternative proteins then? What is behind the ‘hype’? To learn more about this sector you can refer to our proprietary AgriFoodTech taxonomy which entails a lot more.

Curious to learn more about the next FoodTech waves? In the second part of this article, we deep-dive on some areas of FoodTech that are a bit more off the radar, but yet extremely important and impactful.